{kind=link}

Dragon Claws

Stocks were absolutely smoked on Wednesday, especially the tech-heavy Nasdaq.

The Dow (DJI) dropped 504.22 points, or 1.25%, and the S&P 500 (SP500) fell 128.61 points, or 2.31%. But the Nasdaq (COMP:IND) fared worse by far, cratering 654.94 points, or 3.64%.

Why?

I’ll let Yahoo Finance explain:

“Tech stocks took a drubbing on Wednesday after lackluster Alphabet and Tesla earnings stirred up worries that Big Tech’s power to fuel gains is fading…

“Stocks [sank] as investors digest mixed quarterly earnings from Google parent Alphabet (GOOGL, GOOG) and Tesla (TSLA), the first of the ‘Magnificent 7’ mega caps to report. EV maker Tesla’s stock price slid more than 12%, while Alphabet shares dropped more than 5%.

“In aggregate, the Magnificent 7 tech stocks lost more than $750 billion in market cap on Wednesday, the most on record for the group.

“Chip stocks also tumbled… as Nvidia (NVDA) fell almost 7% while Broadcom (AVGO) and Arm (ARM) each dropped about 8%.”

“Barron’s, for its part, adds that, “Investors are also likely double-guessing their take on artificial intelligence and whether the massive investments will see the payoff they’ve imagined.” And as for the larger selloff:

“Former New York Fed President Bill Dudley, meanwhile, said the Federal Reserve should cut rates in July, sparking questions of whether there’s weakness in some pocket of the economy that the markets are missing.”

And so, instead of investigating that concern, investors sold everything. That’s what happens when you’re investing on enthusiasm alone.

Nvidia Is Impressive, But…

Essentially, everyone panicked on Wednesday’s news, turning previous hope-based hype on its head. There’s little else to say about it, except that I’m sincerely sorry for anyone who saw their positions plummet.

On the plus side, all three of the major indices are still very much up year-to-date. So there’s that. And despite its near-7% drop, Nvidia is still a massive winner for anyone who’s held it since January, much less before.

Here it is compared to the rest of the Magnificent 7:

(Yahoo Finance)

The darker blue line, if you can’t see, marks Nvidia’s progress year-to-date. While that other blue line way down at the bottom represents Tesla.

Pink is Google. Orange is Meta Platforms (META). Yellow is Netflix (NFLX). Green is Amazon (AMZN). And purple is Apple (AAPL).

There’s a clear winner here, even with this month’s falls from favor. I’m the first person to give credit where credit is due.

But I’m also still more than content not owning it. Why should I when there are plenty of undervalued, dividend-paying stocks out there I don’t have to second-guess myself about.

This, of course, includes real estate investment trusts, or REITs.

I know real estate suffered on Wednesday too.

The Vanguard Real Estate Index Fund ETF Shares (VNQ), which holds so many of these publicly traded positions, dropped $1.32, or 1.47%.

I’ll also acknowledge that even some high-quality REITs, like Federal Realty Investment Trust (FRT) – a dividend king, for heaven’s sake – dropped over 2.22%. On no news at all!

In which case, it’s clear that, like Big Tech, REITs can experience volatility.

Even so, I’ll take that possibility along with the far smaller share price gains in favor of recurring, rising dividends. That and the fact that, like I said, I can wrap my head around their real value – past, present, and future alike.

My Case Against Owning Too Much AI

I appreciate innovative products and services. There can be real value in companies that cannot just roll with the times, but actually create them.

The possibilities surrounding AI are significant. It could transform education, healthcare, finance, transportation, manufacturing, marketing, entertainment…

Basically, every aspect of our lives could take intense turns for the better with AI adaptions. (They could also take dramatic turns for the worse, but let’s stay positive here.) So I understand why these advancements get investors excited.

Yet, there’s a lot of “could” there that makes me uncomfortable.

Almost two months ago, The Wall Street Journal published a piece titled “The AI Revolution Is Already Losing Steam.” Its tagline: “The pace of innovation in AI is slowing, its usefulness is limited, and the cost of running it remains exorbitant.”

It’s a compelling piece, and – whether it’s ultimately wrong or right – it backs each of those summary points up with paragraphs worth of facts and figures. But it’s the article’s conclusion that really stands out to me:

“None of this is to say that today’s AI won’t, in the long run, transform all sorts of jobs and industries. The problem is that the current level of investment – in startups and by big companies – seems to be predicated on the idea that AI is going to get so much better, so fast, and be adopted so quickly that its impact on our lives and the economy is hard to comprehend.”

That’s why I say Nvidia’s current valuations are hype-based. It’s not to insult the company, what it does, or who believes in it.

It’s simply to say that I want something more concrete.

Like real estate.

Real estate has been around for millennia. And unless we somehow manage to become online entities, it’s going to be around for quite a while more.

Will our exact uses for real estate change? Of course. REITs themselves have added plenty of subsets since first being recognized in 1960.

Likewise, our evaluations of property value fluctuate. But the larger need for brick-and-mortar buildings is pretty much set in stone. It’s something we can count on.

And I, for one, feel comfortable investing in that actuality.

VICI Properties Inc. (VICI)

VICI is a real estate investment trust that owns and operates a portfolio of gaming, hospitality, and entertainment properties across 26 U.S. states and 1 Canadian Province.

The company was formed in 2017 as a spin-off from Caesars Entertainment (CZR). It has grown to become a leading REIT in the gaming industry with a market cap of approximately $31.9 billion and a 127.0 million SF portfolio comprising 54 gaming facilities and 39 non-gaming experiential properties.

The company’s gaming portfolio includes approximately 4.2 million SF of gaming space. That includes over 60,000 hotel rooms, 6.7 million SF of meeting and convention space, over 500 food and beverage outlets, including bars, restaurants, and nightclubs, as well as 500 retail outlets and more than 50 entertainment venues.

Additionally, the company owns 4 championship golf courses and more than 25 acres of undeveloped land next to Planet Hollywood, as well as 7 acres of strip frontage at Caesars Palace.

VICI has gaming properties located in 15 states, but its primary market is Las Vegas, which represents ~47% of its gaming portfolio.

The company has 10 trophy properties on the Las Vegas Strip including Caesars Palace, the Venetian Resort, the Mirage, Park MGM, Excalibur, Harrah’s, and MGM Grand. In total, VICI owns more than 650 acres of land, roughly 41,000 hotel rooms, and nearly 6.0 million SF of convention space on the Las Vegas Strip.

VICI – IR

VICI’s non-gaming portfolio primarily consists of family bowling entertainment centers, which it acquired last year in a sale leaseback with Bowlero Corp (BOWL).

In October 2023, VICI completed the acquisition of the Bowlero Properties for $432.9 million at a 7.3% cap rate.

The initial annual cash rent is nearly $32.0 million with contractual rent escalation equal to the greater of 2.0% or CPI, subject to a 2.5% cap. The initial lease term is for 25 years and has multiple 5-year renewal options.

At the time of the acquisition, BOWL had 2023 pro forma corporate level rent coverage of 3.2x.

Investors had a mixed reaction to the BOWL acquisition, but on the whole I think it was a good move as the concept aligns with VICI’s experiential investment criteria and the purchase further diversifies the company’s portfolio.

Moreover, it adds a new tenant operating in a new sector, and adds new assets across 17 states, including 11 states that are new to VICI.

VICI – IR

VICI leases its properties under long-term, triple-net lease agreements, which provide stable and reliable cash flows with long-tern visibility. The triple-net lease structure also makes the operator responsible for expenses such as property tax, insurance, and maintenance.

All of VICI’s leases are triple-net and more than 90% have a parent guarantee in place. Additionally, 81% of its rent roll includes master lease protection and 80% of its rent roll includes tenants that report to the Securities & Exchange Commission (“SEC”).

VICI’s leases are structured on a very long-term basis. When including extension options, its portfolio has a weighted average lease term (“WALT”) of 41.5 years. This provides for stable income with long-term visibility while minimizing VICI’s operating expenses.

The company’s tenant roster has many favorable attributes, but it is very concentrated, with only 13 tenants. Furthermore, it is especially concentrated in its top 2 tenants, Caesars Entertainment and MGM Resorts, which combined make up roughly 74% of VICI’s annual rent. Normally, I’d run from such tenant concentration, but in VICI’s case, the situation is unique.

VICI is one of the few REITs I consider to have a true defensive moat due to the iconic nature of its properties. A tenant can easily move to a different retail outlet, or to a different shopping center, but Caesars Palace on the Las Vegas Strip is virtually irreplaceable.

CZR would find it very difficult to operate without the real estate supporting its operations. The company cannot just up-and-move on a whim, and would likely go to great lengths to keep its place on the Las Vegas Strip.

A convenient store operator has many options on what property it leases, but a gaming operator that needs high-class amenities, hotel rooms, restaurants, and an iconic destination does not.

The last thing I’ll say regarding its tenant concentration is that these are very well capitalized companies with deep resources. Especially its top 2 tenants, Caesars and MGM Resorts. While I never like high tenant concentration, in VICI’s case there are features that mitigates the risk.

The moat surrounding VICI has helped the company maintain 100% portfolio occupancy and achieve 100% rent collection since its formation.

VICI – IR

Another interesting aspect of VICI is the speed at which it went from a spin-off to an S&P 500 company with an investment grade balance sheet.

As previously mentioned, VICI was spun-off in 2017 from Caesars Entertainment and received several assets operated by Caesars as part of the deal. The company acquired Harrah’s Las Vegas in 2017 before completing its initial public offering (“IPO”) in 2018, which was the 4th largest REIT IPO on record.

Later that year, it expanded its tenant roster with the addition of PENN Entertainment and continued to diversify its tenant base with the additions of Hard Rock, JACK, and Century Casinos in 2019. Over the following years, the company grew through investment and acquired many key properties, including Chelsea Piers and the Venetian Resort.

By 2022, just a handful of years after its spin-off and IPO, the company was included as an S&P 500 member and earned an investment grade credit rating (BBB-).

Since then, VICI has continued to invest and expand its portfolio. Last year, the company acquired the remaining 49.9% interest in the MGM Grand / Mandalay Bay and added a new vertical with its acquisition of the Bowlero properties.

In total, from the 2017 spin-off to 1Q-24 annualized, VICI has grown its adjusted EBITDA by roughly 330%.

VICI – IR

The rapid growth of VICI’s portfolio has been accretive and is reflected on the bottom line. The company has an average Adjusted FFO (“AFFO”) growth rate of 6.77% and an average dividend growth rate of 10.11% over the past 5 years.

Analysts expect AFFO per share to increase by 5% in 2024, and then increase by 4% in both 2025 and 2026.

FAST Graphs (compiled by iREIT®)

VICI has an investment grade balance sheet with a BBB- credit rating from S&P Global and solid debt metrics, including a net leverage ratio of 5.4x (net debt / adj. EBITDA), a long-term debt to capital ratio of 40.82%, and an EBITDA to interest expense ratio of 4.19x.

The company’s debt is 83% unsecured and 99% fixed rate. At the end of the first quarter it had approximately $3.5 billion in liquidity, and the company’s debt maturity schedule is well staggered with a weighted average term to maturity of 6.8 years.

VICI – IR

VICI is a triple-net lease REIT that should continue to generate stable and reliable cash flows for the long term. The company’s properties are experiential, which insulates it from the threat of e-commerce, and iconic, which gives the company a true defensive moat.

VICI has grown at a rapid clip since its formation, while maintaining a conservative capital structure and a fortified balance sheet. Demand for the Las Vegas experience should continue to grow, and legal gambling is not going anywhere.

VICI pays a 5.46% dividend yield that is well covered with a 2023 AFFO payout ratio of 74.88% and its stock is trading at a P/AFFO of 13.80x, compared to its average AFFO multiple of 15.93x.

We rate VICI Properties a Buy.

FAST Graphs

Terreno Realty Corporation (TRNO)

TRNO is an internally managed REIT based out of San Francisco that specializes in the acquisition and management of industrial real estate across 6 major coastal markets which include: Los Angeles, New Jersey / New York City, Miami, Seattle, San Francisco, and Washington, D.C.

The company has a market cap of approximately $6.7 billion and a 17.4 million SF portfolio comprising 290 industrial properties and 45 improved land parcels totaling 152.4 acres, as well as 1.6 million SF of properties under development or redevelopment.

Terreno looks to acquire functional and flexible industrial properties in infill locations that are located in high-demand, supply constrained markets.

The company also targets locations that are near large population centers and transportation hubs and looks for properties that can serve multiple tenants and support distribution, e-commerce, and general logistics activities.

TRNO’s portfolio includes various industrial properties and other assets including warehouse / distribution, flex / light industrial, transshipment, and improved land.

The company receives roughly 76.8% of its annualized base rent (“ABR”) from its warehouse / distribution properties, which include single and multiple tenant facilities that are typically larger than 10,000 SF.

Terreno derives roughly 12.4% of its ABR from its improved land that is used for industrial outdoor storage, which can include truck, trailer, and vehicle parking. These improved land parcels are also held as they may be redeveloped at opportunistic times.

The company receives 7.1% of its ABR from its transshipment facilities, which are shallow bay industrial parks. They can serve both single and multiple tenants with a high number of dock-high doors that can facilitate efficient loading and unloading of goods.

TRNO receives approximately 3.7% of its ABR from its flex properties, which are normally less than 10,000 SF and accommodate warehouse, light-industrial, and manufacturing activities and generally include some amount of office space.

At the end of 1Q-24, the company reported a same-store portfolio occupancy of 96.2%.

TRNO – IR

Earlier this year, Fitch Ratings upgraded TRNO’s long-term issuer default rating from BBB to BBB+ (Stable).

The company attempts to maintain financial flexibility and a conservative capital structure. With a long-term debt to capital ratio of 17.52%, the company has a very conservative capital structure, as equity makes up more than 80% of the company’s capital.

The company has excellent debt metrics, including a net debt to EBITDA of 3.17x and an EBITDA to interest expense of 7.77x.

As illustrated below, the company has been improving both its leverage and coverage ratio over the last several years.

Back in 2016, the company had a leverage ratio (net debt to EBITDA) of 6.98x and a coverage ratio (EBITDA to interest expense) of 4.40x. Both metrics have steadily improved, with the leverage ratio trending down and the coverage ratio trending up.

TIKR.com

Terreno Realty has been a growth machine over the last decade, with an average AFFO growth rate of 14.28% since 2014. Over this period, the company’s AFFO per share has had positive growth in each year except 2015, when AFFO per share fell by -10%.

Analysts expect robust growth over the coming years, with AFFO per share projected to increase by 9% in both 2024 and 2025, and then increase by 17% the following year.

FAST Graphs (compiled by iREIT®)

Below is a list of the AFFO growth rates Terreno has delivered over the last decade. I excluded the 63% growth rate (2014) from the chart so it could be scaled without too much distortion:

- 2014: AFFO +63%

- 2015: AFFO -10%

- 2016: AFFO +19%

- 2017: AFFO +11%

- 2018: AFFO +30%

- 2019: AFFO +8%

- 2020: AFFO + 2%

- 2021: AFFO + 1%

- 2022: AFFO +15%

- 2023: AFFO +27%.

FAST Graphs (compiled by iREIT®)

Terreno and the rest of the industrial sector should continue to benefit from the growth and increasing adoption of e-commerce.

As online retail continues to grow, it will result in more demand for industrial space near urban areas, and TRNO is well-positioned to take advantage of this trend.

TRNO is in a fast-growing sector with a long runway for continued growth. The company has excellent debt metrics and is in a solid financial position to support its investments for future growth.

The company pays a 2.61% dividend yield and has an average annual dividend growth rate of 10.85%. Dividend coverage has been a bit tight over the last several years, with an AFFO payout ratio exceeding 100% in 2021 & 2022 and a 2023 AFFO payout ratio of 96.59%.

However, if analysts’ projections are on the mark, the company’s AFFO payout ratio will improve to 94.26% in 2025 and then to 87.70% in 2026.

Currently, the stock is trading at a P/AFFO of 37.21x, compared to its average AFFO multiple of 40.99x.

We rate Terreno Realty a Buy.

FAST Graphs

In Closing

As the author of REITs for Dummies, you know that I’m super bullish on REITs.

In addition, I’ve been a real estate investor for over three decades, so I have seen my fair share of market cycles.

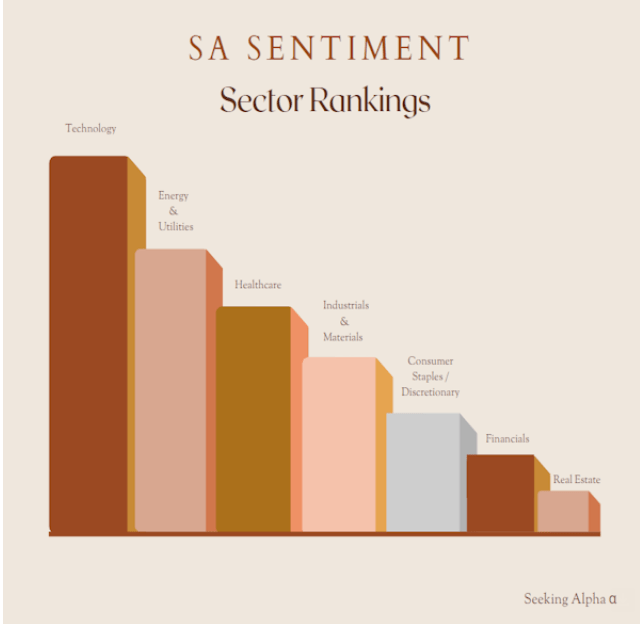

As you can see below, market sentiment for REITs is low:

Seeking Alpha

In my view, NOW is a great time to buy REITs, while sentiment remains low.

The legendary long-term investor Warren Buffett has said that it is better to be fearful when others are greedy and greedy when others are fearful. Value investors like me (and Buffett) tend to be contrarian.

And as a real estate investor, I have always lived by these words,

Buy Low, Sell High

As always, thank you for reading and commenting.