{kind=link}

When investors think about municipal bonds, safety and stability often come to mind. Afterall, a city or state government has the ability to tax their citizens to help pay for the bonds. As a result, munis often form the cornerstone of many conservative fixed-income investor’s portfolios. But not all munis are safe and steady, some are a tad on the risky side. But for investors looking to pick up extra yields, these bonds could be a real opportunity.

Today, that opportunity lies within munis tied to senior living and nursing homes.

The senior living sector has long been one of the riskiest in the high-yield muni space — skewing default rates higher for all muni bonds. Those issues have only gotten worse since the pandemic. But with an aging population and increased elderly care needed, the sector could provide an interesting blend of risk and reward for some income seekers.

The Riskiest of the Risky

Municipal bonds are issued by state and local governments as well as their entities. As such, when investors tend to think about municipal bonds they think about so-called general obligation (GO) bonds. The ability to repay these bonds is directly tied to the State of Texas’s or City of Sacramento’s ability to tax its citizens and businesses.

However, the muni market is a two-sided coin.

And here, the other side is a larger share of the pie. Revenue-backed bonds are tied to specific projects. These bonds are issued to fund essential services that are financially independent of the city, county or state they serve. They are repaid by the revenues generated from the project. Some examples include mass transit, utilities and even sports stadiums/concert venues.

Senior living facilities fall within this category.

These bonds are issued by governments to finance construction of senior living facilities, such as nursing homes, assisted living facilities, continuing care retirement communities, and memory care facilities. States and local governments get involved to meet the needs and to entice private owners. Owners of the facility pay back the bond based on the revenues they generate. But, factors such as occupancy rate, operating costs, competition and, ironically, enough government regulation can impact revenues. And if that cash is insufficient to cover the debt service payments, the bondholders may face a default.

And they do default.

As of the end of the first quarter of this year, more than 8% of senior living munis were in default. In 2023, the default rate for the senior living sector was a whopping 10.8%. To put this in perspective, looking at the entire municipal bond sector, the default rate is about 0.41%.

COVID-19 certainly has added additional pressures on the sector. Apart from the impacts of the pandemic, the senior living sector is, by far, the leading area where defalts happen within the muni space.

Why Take on the Risk?

So, why even bother with the sector? For starters, yields for senior living bonds are some of the highest in the municipal space. You are talking 5% to 8%. That’s a pretty juicy yield no matter how you slice it, and is on par with regular junk bonds before muni’s tax advantages kick in. For income seekers, it’s an easy way to boost a portfolio’s yield.

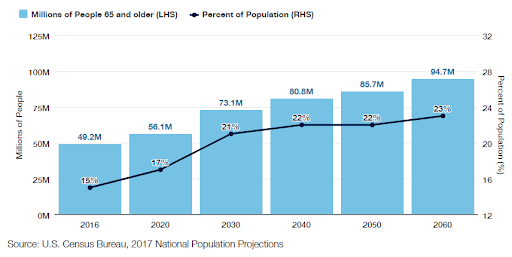

Another reason to consider senior living munis? Our aging population. Demand for senior living and elder care is only growing. In roughly five years, according to the U.S Census Bureau, the U.S. population will hit an inflection point. It’s at that point in time that the massive Baby Boomer generation will hit 65. By 2040, nearly 81 million people will be of retirement age in the U.S., representing 22% of the population.

Source: Thornburg

As modern medicine increases our lifespans, it’s putting a strain on elder care needs. According to asset manager Thornburg, this is wonderful news for the senior living bond sector. Cash flows for these bonds should only strengthen as more people begin to use these services. Moreover, COVID-19 and the issues from the pandemic put the kibosh on construction activity and issuance of bonds. The reduction in the number of facilities is bullish for the rents and cash flows of existing centers. And with less bonds being issued, those that are will be in greater demand.

For investors today, this reverses the whole risk-reward equation. Yes, they are risky, but the longer term seems rosy as demand increases. This risk-reward equation is highlighted by the fact that default rates have continued to decline in recent months. Investors may be buying more reward with even less risk than just a year ago.

Betting Big on the Aging Population with Senior Living Loans

Now, senior living bonds are still risky when compared to the overall muni market, and even the high-yield muni market for that matter. But for those investors looking to juice their income or who are younger and can take on more risk, they could make sense. Longer term, they have plenty of reward.

The question is how to buy them.

Buying individual municipal bonds is a challenging proposition without certain state government bonds. And given the extra risks associated with senior living bonds, investors may want to stay clear of them individually.

Luckily, as a major part of the high-yield category, senior living bonds feature prominently in many ETFs that track the sector. Sadly, there aren’t any muni bond ETFs that track different segments of the space … yet. Active management could be key in finding senior living bonds with great risk-reward prospects.

High-Yield Municipal Bond ETFs

These funds were selected based on their exposure to the high-yield municipal bond market. They are sorted by their YTD total return, which ranges from 3.4% to 9.9%. They have assets under management between $82M and $2.92B and expenses between 0.32% and 1.82%. They are currently yielding between 1.8% and 5.1%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| XMPT | VanEck CEF Muni Income ETF | $239M | 9.9% | 5.6% | 1.82% | ETF | No |

| HYMU | BlackRock High Yield Muni Income Bond ETF | $82M | 7.1% | 4% | 0.35% | ETF | No |

| HYMB | SPDR® Nuveen Bloomberg High Yield Municipal Bond ETF | $2.59B | 5.7% | 4.3% | 0.35% | ETF | No |

| FMHI | First Trust Municipal High Income ETF | $573M | 5.5% | 4% | 0.70% | ETF | Yes |

| JMHI | JPMorgan High Yield Municipal ETF | $175M | 4.9% | 5.1% | 0.59% | ETF | Yes |

| HYD | VanEck High Yield Muni ETF | $2.92B | 4.5% | 4.4% | 0.32% | ETF | No |

| SHYD | VanEck Short High Yield Muni ETF | $329M | 3.4% | 3.3% | 0.35% | ETF | No |

While the previous funds aren’t pure vehicles, they do include senior living bonds in their holdings — and that might be enough to help boost yields and total returns. For investors, the sector is risky, but there are tailwinds that help propel it forward. Thinking broadly could be their best bet.

Bottom Line

Senior living municipal bonds have long been the place for high default rates amid high yields. But the risk-reward proposition could be changing. And the aging population could be strengthening the cash flows for these facilities. This is bullish news for these municipal bonds and their investors.