{kind=link}

VanderWolf-Images

RTX (NYSE:RTX) may not be a top pure play in defense given it’s only 40% of the backlog, but in my view, is fundamentally a more defensive (non-cyclical) play than the average stock in the current market environment. The business has a strong set of commercial operations and remains exposed to the bullish trends of growing defense spending, especially in Europe. Revenue growth on fixed costs, as well as some cost restructuring, is also expected to drive margin growth for all divisions in 2024. Valuation is fair given the level and nature of growth. However, a significant concern lies in the company’s poor cash use, leading to a leveraged balance sheet that translates to high interest expenses impacting EBT. Investors should closely monitor execution in this regard.

Favorable Backdrop for Defense

The outlook for defense-related stocks remains bullish. European stability remains a major concern, and the growing risks of a Chinese invasion of Taiwan underscores the need for increased defense investment. Europe, in particular, is seeing a strong increase in defense spending, with many NATO countries reaching the 2% GDP target and in some cases surpassing it (such as the UK announcing a 2.5% target, or Poland surpassing 3%).

With the markets broadly overextended, I believe exposure to the defense sector offers advantages in terms of less cyclical and more idiosyncratic structural trends. While RTX may not be a pure play in this space due to its $125bn commercial backlog out of a total of $202bn, it still has ~40% of its backlog in defense, and it’s embedded in key defense platforms such as Patriot missile systems, GEM-T, NASAMS, SPY-6 radars, AMRAAM, Tomahawk and the Standard Missile family. As Russia’s war on Ukraine continues, NATO countries are providing an increasing number of Patriot missile systems to Ukraine, necessitating future replacements to maintain proper domestic air defense capabilities. Patriots form the backbone of air defense for 19 countries, including Germany, the U.S. and Ukraine, and many of RTX’s products are embedded in current NATO defenses.

Strong Growth In Commercial, Idiosyncratic Growth in Defense

RTX is experiencing strong growth with a record order backlog of $202bn (nearly three years of revenue) and a very good book-to-bill of 1.34x, suggesting continued revenue expansion. Organic sales for Collins Aerospace are growing at a 9% rate (Q1’24) while Pratt & Whitney is expanding at an impressive 23% rate. Commercial aftermarket sales were up 11% year-over-year in Q1’24, with Collins up 14% and Pratt up 9%.

I believe these represent very solid growth rates for a business of this size. Defense via Raytheon appears to be growing more slowly at a 6% rate. However, I believe investors should recognize the more defensive nature (less cyclical) of these revenue streams due to the idiosyncratic trends in defense spending (especially in Europe) which arguably don’t rely much on the business cycle (Europe needs to bolster its defenses somewhat independently from economic fluctuations). The book to bill at 1.05x in the division is not particularly exciting and is slightly down versus the 1.09x reported in Q1’23, but some volatility is a normal occurrence given the volatility in order cycles. Regardless of what might be short-term volatility in order books, demand for Raytheon products from US allies persists and aid to Ukraine, as well as reinforcement of domestic defenses, continue to be a driver for new orders. For example, Raytheon was awarded a $1.2bn contract to supply Germany with additional Patriot air and missile defense systems, which follows the country’s pledge of three out of eleven of its existing Patriot systems to Ukraine.

Collins Aerospace and Pratt & Whitney exhibit a more cyclical due to the exposure to commercial, regional and business aircraft besides military ones, yet they both have a very sound competitive position and long-term drivers of revenue.

-

Collins is number one or number two on 70% of its product portfolio and has an off-warranty installed base of $100 billion, which can create decades of aftermarket growth.

-

The large commercial engine business at Pratt has an installed base of 12,000 engines and a backlog of over 10,000 GTF (geared turbofans), which can also fuel long-term growth. Moreover, Pratt & Whitney’s small engine business has sole positions in ~63,000 engines in services, offering streams of aftermarket revenue.

Structurally, the exposure to the market-share-gaining Airbus is also a positive driver that could propel continued outperformance, especially if Boeing’s recent operational issues persist. The Pratt & Whitney GTF engine family powers several popular Airbus aircraft models, including the A320neo family and the Airbus A220.

Margin Expansion and Bullish Outlook

RTX’s margin trends were underwhelming in Q1’24, but the firm still expects to experience margin growth thanks to economies of scale on fixed costs, and some benefits from cost reduction programs. However, the bottom line is experiencing pressure from growing interest expenses which, in my view, is due to poor capital allocation more than macro conditions.

EBIT Margin Expansion But Pressure From Interest Expense

A positive aspect of having a high fixed-cost business is the ease of margin expansion when volumes and revenue grow due to strong demand. The adjusted operating profit margin at the group level was down ~20bps YoY in Q1’24 (dragged by Pratt & Whitney in particular) but management maintained a positive outlook for the rest of the year, expecting volume increases to drive continued fixed cost absorption benefits in 2024. RTX is also working on cost reduction measures to further expand margins, such as an additional 400,000 manufacturing hours expected to be moved to best-cost locations.

Cash Use and EBT pressure

The business is rationalizing its portfolio with the recent $1.3bn divestiture of Raytheon’s cybersecurity, intelligence and services business, which gives fresh cash to strengthen the balance sheet and offer resources for capacity expansion.

RTX announced $3 billion in company-funded R&D for 2024, plus $5 billion in customer-funded R&D to develop new technologies and products. The business is also expanding capacity in key areas to meet customer demand, as part of its $2.5 billion capex expected in 2024.

Strengthening the balance sheet should be, in my view, the preferred path, given the business now spends around $2bn per year in interest expense, which amounts to over a quarter of annualised EBIT. This is relatively high compared to other defense stocks (e.g. Lockheed Martin (LMT) had interest expenses at ~12% of EBIT last quarter). A better balance sheet could also come as a result of high-margin growth leading to strong cash flow generation, but the firm’s cash use has been concerning in recent times. In FY’23, the business issued a net $12.4bn of long-term debt and contextually bought back almost $12.9bn of common stock. I think this was a very poor capital allocation choice, and it’s expected to contribute to a big increase in interest expense from $1,505m in 2023 to $2,050m in 2024.

Outlook Is Bullish

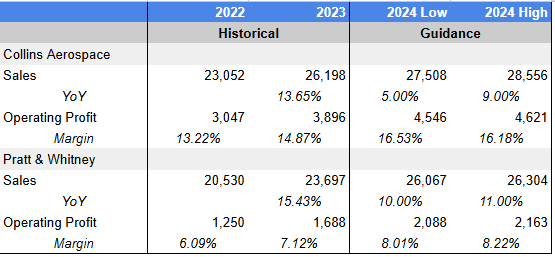

RTX’s segment outlook highlights ongoing positive prospects for Collins Aerospace and Pratt & Whitney, both expected to experience strong growth at high profitability. Trends at Raytheon are expected to remain relatively weaker, with only low to mid-single-digit organic growth expected in 2024. Adjusted sales are expected to be down to flat due to the divestiture of the cybersecurity business, but operating profit in the division is expected to expand by $100m – $200m including a $80m headwind from the sale of the cybersecurity business, implying a significant margin expansion.

Q1’24 Presentation

Trying to put the guidance in actual numbers suggests that both Collins Aerospace and Pratt & Whitney are expected to experience some operating margin expansion as well.

Author, Company Filings

Valuation – Not A Bargain, But Fair Multiples For Quality Growth

An assessment of RTX’s valuation must take into account factors such as the relatively defensive nature of nearly half of the business, the positive underlying trends in the medium term, and the margin expansion expected to occur on the back of revenue growth. Consensus EPS estimates of $5.38 for 2024 are within the $5.25 -$5.40 guidance and appear reasonable in my view, implying a 2024E P/E ratio of less than 20x, a discount to the 24x for the S&P 500.

As a capital-intensive business experiencing growth, FCF is compressed by capex and FCF multiples are consequently higher. RTX is currently at ~25x management’s 2024E FCF guidance of $5.7bn. At a discount rate of 9% and 3% terminal growth, RTX needs to deliver 10% CAGR in the next six years to justify its valuation, which isn’t an overly demanding hurdle. Even assuming minimal idiosyncratic factors specifically impacting RTX, the Aerospace industry is expected to grow at a CAGR of nearly 6%, similar to defense. With a particular exposure to NATO’s growing defense spending and positive drivers in aerospace, a medium-term revenue CAGR of 6-7% with some margin expansion driven by economies of scale on the fixed cost base seems definitely achievable. Moreover, proper use of cash to de-lever the balance sheet would create a virtuous cycle of further earnings and FCFE growth as well.

Conclusion

In a seemingly overextended stock market with growing downside risk, I believe there are areas where the risk/reward is still favorable, such as defense. While RTX may not be a pure play on this theme, I think the exposure to high-quality defense platforms positively skews the risk-reward from a fundamental perspective. The company exhibits solid growth trends supported by structural trends, together with an outlook of meaningful margin expansion and strong cash flows. It also comes at a reasonable valuation, with the stock showing momentum while reaching all-time highs. I think RTX is still worth a shot at these levels, although with caution and with an eye on execution given the red flags in leverage and cash use.