")

{kind=link}

DusanBartolovic

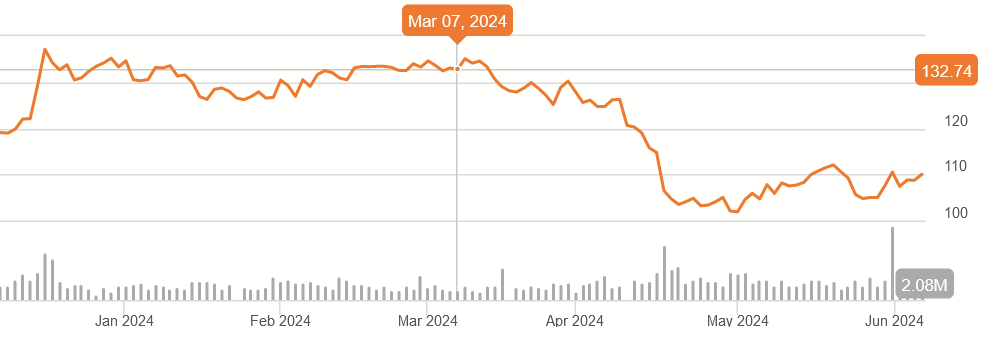

Many REITs currently trade, at their lowest, around a 5% dividend yields, roughly a money market’s interest rate. Prologis (NYSE:PLD), meanwhile, trades at 3.5%, and this is even after almost a 15% dip from recent highs in March.

PLD 6M Price History (Seeking Alpha)

This relative premium is worth examining. Is it paying more for dependable cash flow, perhaps valuable properties? Is there a growth story?

If people like the safety, maybe they can buy it, but I’m concerned the price reflects old growth and not new. For that reason, I’m rating this a Hold.

Financial History

Over the past decade, Prologis has been a rapidly growing business.

Author’s display of 10K data

Revenues are up more than 4x over the past decade, indicating not only good rent collection but a fast-paced pipeline of acquisitions. Keep in mind that this counts reported revenues plus earnings from unconsolidated entities.

Author’s display of 10K data

As it relates to the cash flow situation, this has also been growing. Both Funds From Operations and Prologis’s figure that eliminates one-time events or cash flow not attributable to the common (which they call Core FFO), are well in excess of their total cash dividends paid. Crucially, cash flow was not interrupted by the COVID pandemic, the war in Ukraine, supply chain disruptions related to both, or the more recent interest rate hikes, indicating a strong real estate portfolio.

Capital Raises (Author’s Display of 10K data)

Unsurprisingly, this growth has not been purely on their original capital but through subsequent raises of long-term debt and new equity. Most of this occurred in the latter half of the decade. LT debt is up about 3x, while total shares outstanding grew 81%.

Annual Dividend 10Y History (Seeking Alpha)

PLD’s annual dividend per share (which is the important part for us), grew from $1.32 in 2014 to $3.48 in 2023, a CAGR of about 11%, which is very good.

10Y Yield History (Seeking Alpha)

Ultimately, we can now appreciate why the yield today and over the past decade has never been over 5%, even in the midst of the COVID crash. This REIT has functioned as a growth investment, and yield on cost for an investment ten years ago is over 9%!

Before we ponder if there is still a growth story, let’s look more closely at the way this business works.

Business Model

Prologis describes itself as an owner and manager of real estate properties that serve some kind of role in logistics and supply chains. It breaks its operations down into three segments: Rental, Strategic Capital, and Development.

Income Statement (2023 Form 10K)

In the table above, Development is a very minor piece of the picture, so I’ll mainly focus on the first two segments.

Rental Properties

Prologis owns a global real estate portfolio, primarily concentrated in North America and Europe.

June 2024 Investor Conference

Their “logistics real estate” mainly consists of strategically situated warehouse space.

June 2024 Investor Conference

Their properties in particular have been oriented toward logistics for the storage and shipping needs of e-commerce, which has seen heavy growth over the past decade and continues to grow. As Q1 2024 (pg. 31), the average lease term for the real estate portfolio was just under five years.

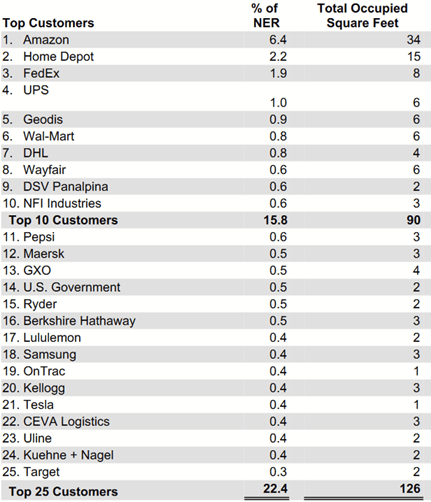

Top 25 Customers (2023 Form 10K)

The portfolio is heavily diversified across many tenants, with the Top 25 representing only accounting 22.4% of Net Effective Rent (“NER”) as of 2023. Many of those names are recognizable, public companies. With a few exceptions, these tenants enjoy consistently positive cash flows from operations over many years, indicating strong ability to cover lease expenses within the portfolio.

Strategic Capital

This involves asset management of real estate through joint ventures with global investment partners, mostly for properties outside of the United States. As such, the income from this segment is not rent but fees earned for the services they provide to the owners.

Q1 2024 Company Presentation

These revenues are one part fee-related earnings (essentially the expense ratio for AUM) and another part what they call “promote income.” This is incentive-based income, earned at the end of specific periods for each venture and thus are lumpier in their contributions to revenue. Seen above, there has been almost no Promote Income YTD 2024.

Balance Sheet

While the spike in LT debt I mentioned earlier might have alarmed some folks, Prologis actually enjoys a pretty healthy balance sheet.

Q1 2024 Form 10Q

The company reports $88 billion in real estate, on top of only $29.6 billion in debt.

Q1 2024 Form 10Q

Drawing from many sources, the debt also enjoys a long, weighted-average maturity of 9.6 years, with interest at an attractively low 3%, thanks to capital raises that preceded rate hikes.

Future Outlook

With interest rates higher than they were during the runway of Prologis’s past growth, that has an effect on future growth, so let’s consider the trends, good and bad, that will inform a reasonable valuation for PLD.

Acquisitions

Prologis had about 1,600 buildings in 2014 and has (as previously shown) over 5,000 today. The natural question is if future acquisitions at a similar growth rate are possible. Can they have 15,000+ warehouses and similar assets in ten years? Moreover, would higher interest rates even make them worth acquiring?

At the recent June Investor Conference, company President Dan Letter had to say:

Well, Southern California has been the best market for Prologis probably for any REIT, if you look over the last 20 years, we will continue to invest in Southern California…but we are going to stick to our discipline, and we are going to be very focused on quality and location. And certainly, we’ll take it through our returns filters, and we are going to make sure that maybe right now, we want to be more opportunistic down there.

Obviously, every allocation of capital is supposed to be “opportunistic.” Otherwise, why do it? This takes some clever interpretation, but I’ve noticed that management from many companies use the word itself more when they don’t see a lot of great buys, and so an actual opportunity becomes the exception, rather than the norm. I think that’s what Letter is expressing here.

This isn’t surprising, given that the obvious choices were already bought over the last decade and when the cost of capital was lower. I expect the near-term growth through acquisitions to be lower and that this will likely be the case until interest rates are lower.

Existing Properties

Management did, however, point to income growth opportunities with the existing portfolio. CFO Tim Arndt explained in Q1 earnings:

As always, we are actively looking at acquisition opportunities across all of our markets, but our focus remains on the development of our land bank, which provides an opportunity for over $38 billion of build out with a return on incremental capital of approximately 8.5%.

June 2024 Investor Conference

There are three components to this effort: expanding the square footage of the properties, conversion of some assets to data centers, and installation of solar panels to satisfy electrical needs of tenants. I believe these are prudent uses of capital, given elevated interest rates and the room for long-term increased value for the properties, so this can help income grow on top of what organic rent increases would be.

Main Risk

Some might wonder about geopolitical risks, but only the concerning country to which they have some exposure is China, and it’s not significant. (Again, trends in Southern California would matter more than anywhere else.)

Rather, I think biggest risk to Prologis, more as it would slow growth, is a decrease in consumer spending that might weaken e-commerce and thus demand for ever-expanding logistics to support it.

The COVID recession had the effect of boosting e-commerce because brick-and-mortar stores were a No-Go, amid lockdowns and social distancing. A more traditional recession, where consumers are strained by something like higher prices, is a different problem. When the CEO of McDonald’s (MCD) warned in April that consumers were feeling the squeeze of inflation, that stood out to me. When the people known for making bargain burgers are worried, I consider it worth listening.

While we’re not at a turning point like that yet, interest rates remain elevated for a reason. Inflation hasn’t cooled down to the Fed’s satisfaction, and the macro-section reflects a uneasy balancing act. For these reasons, some caution is warranted on the part of investors looking for a long-term stake in PLD.

Valuation

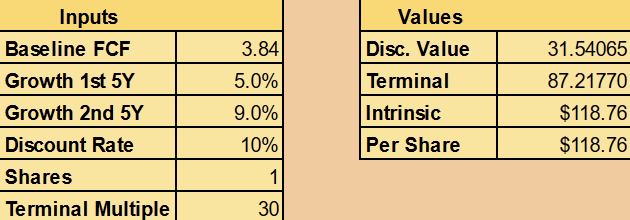

For my valuation, I will use a method similar to Discounted Cash Flow, substituting free cash flow with the annual dividend per share. I will make the following assumptions.

- 5% growth the first 5 years

- 8% growth the next 5

- Terminal multiple of 30

5% growth reflects current guidance by management provided in the June Investor Conference on expected, global rent growth for the next few years. I believe growth can speed up afterward, after interest rates decline and allow for easier acquisitions, along with the realization of the capital improvements to the existing portfolio. Given the size of Prologis now, I have doubts it will be that same 11% CAGR again. A terminal multiple of 30, meanwhile, reflects a typical yield at which PLD trades.

Author’s calculation

For a 10% discount rate (typical return of a broad market index), this suggests that a fair value per share is about $119, making the current price of $110 slightly undervalued.

Having said that, growth rates could be hindered by the risks I mentioned. Moreover, the market might sour if growth perceptions do not last in the future, so much of this valuation depends on a favorable yield/multiple. Long-term investors should take that into account.

Conclusion

Prologis has spent the last decade creating a solid real estate portfolio at an impressive CAGR. With a diverse array of cash-flow-positive tenants who operate in a growing industry of e-commerce, the business can continue to ride that wave and pass the rewards to shareholders.

The real question is if growth will be what it was in the past. With higher interest rates and acquisitions now just being “opportunistic,” that’s less wind in the sails. Capital improvements to the existing properties are a good move, but their ultimate benefit will take at least a few years to be realized and may not match previous boons of expansion and rent hikes.

Prologis represents a safe REIT, and that might explain its low yield, but the long-term returns are going to depend on how well it grows now that conditions have changed. Since the main issue is that the price doesn’t scream an obvious discount for slower growth prospects, I have to consider it a Hold for now, albeit a decent one.