RiverRockPhotos

Summary

Grupo Mexico SAB (OTCPK:GMBXF) or GMEX, is a promising holding firm for the future as it operates in three key sectors for the green and electrified future, very aligned with the big tailwinds that will unfold in the following years. The management operates in a very solid financial way using their long experience in history and always rewarding their shareholders, delivering solid returns for them.

Currently, the stock is trading at fair value. Its weak point is the excessive dependence on the copper price, so I prefer to keep this name on my watchlist waiting for future pullbacks as the world economy is presenting some symptoms of cooling down. This article seeks to give readers a complete company analysis, providing them with context and historical references, helping them to understand the past, present, and future of the firm before deciding whether to add this name to their portfolios.

Business Overview

Grupo México, S.A.B. de C.V. is a global firm with a long history going back to 1890, when the first subsidiary, Asarco, started its mining activities in Mexico. During these 130+ years of history, the firm has expanded its operations into new markets and sectors as transport and infrastructure.

Company 2023 Annual Report Company 2023 Annual Report

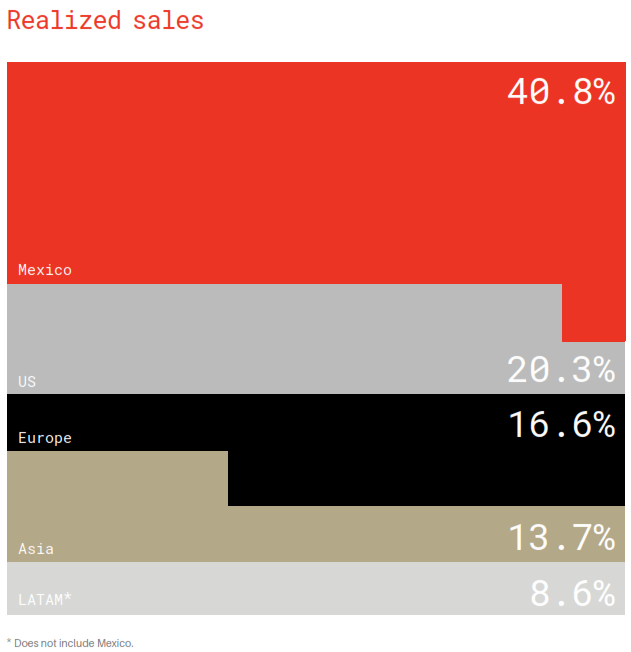

For the year 2023, 40.8% of its activities were accounted for Mexico, 20.3% for the US, 16.6% for Europe, and 13.7% for Asia, the rest 8.6% of the sales came from a mix of LATAM countries including Peru, Ecuador, Chile, and Argentina among others.

Company Structure

{kind=link}

{kind=link}

Mining Division: Americas Mining Corporation. This segment accounts for 75.6% of sales and 81.6% of the net profit for the group in 2023. GMEX operates this division controlling 88.9% of Southern Copper Corporation (SCCO), 100% of ASARCO, and 97.3% of Mineras Los Frailes. Together, these companies produce mainly copper, but also zinc, silver, gold, and molybdenum. These companies have one of the lowest operational costs in the industry. They have the biggest copper reserves and resources in the world. These three companies together represent the 4th copper producer worldwide. Their operations are based mainly in Mexico (59%) and Peru (41%).

Transportation Division: Grupo Mexico Transportes (OTCPK:GMXTF). This segment contributes to 21.7% of sales and 16.6% of the net profit for the group in 2023. This part of the business is centered on managing and operating 11,137 km of rail track in 24 Mexican states, Florida, and Texas. They also operate rail connections with 5 ports in the Pacific, 4 in the Gulf of Mexico, and 4 on the Atlantic.

Infrastructure Division: Mexico Proyectos y Desarrollos. This segment contributes to 2.7% of sales and 1.9% of the net profit for the group in 2023. The company has 80 years of experience in building infrastructure and industrial plants. They also cover engineering services mainly in Mexico but also abroad. Some of their infrastructures are modular platforms, jack-up rigs, a combined cycle plant at La Caridad delivering 500 MW, 2 wind farms one at El Retiro, with 37 turbines delivering 74 MW, and one at Fenicias with 42 turbines delivering 168 MW. They operate 2 highways, one in the section between Salamanca-León (80 km) and Libramiento Silao (17.4 km).

Financial Position & Performance

Units expressed in millions of US dollars. All the information shown has been extracted by the author directly from the annual reports of the company.

P&L

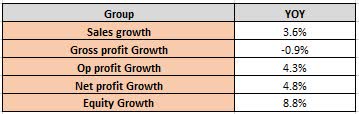

The company has grown both top and bottom line in 2023. But, if we take a deeper look into the division’s performance we can see some more interesting aspects:

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

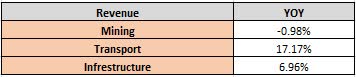

First of all, the Mining division lags a bit in revenue growth, as it was almost flat YOY. Instead, the Transport division managed to increase its revenue by 17.17% as the Infrastructure segment grew by 6.96%.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

And, as we can see below, in 2023 81% of the net profit came from the Mining division, instead in 2022 it was 83%. On the other hand, Transport and Infrastructure divisions contribute 17% and 2% respectively.

Image created by the author using information from the company´s annual reports (Author’s own Analysis)

Regarding margins, YOY in general, the group managed to maintain its operating and net margin, but the gross margin decreased by -4.3%, mainly because of the higher costs that the Mining division suffered.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

The Transport division did well, keeping margins almost constant, and the Infrastructure segment managed to improve all the margins across the board, contributing to the group’s good result in the bottom line.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis) Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

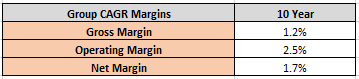

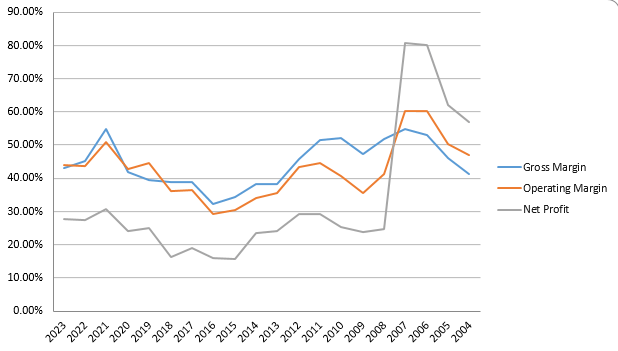

In the last 10 years, Grupo Mexico has managed to improve its margins steadily, which indicates that the firm has the strength and resilience to navigate the commodity cycle.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

However, in the last 3 years, GMEX has struggled to keep the group’s historical growth rate, higher inflation has increased the costs and the firm has struggled to contrast these factors with higher volumes of sales. Also, having +80% of the sales coming from a commodity sector means that the group has no pricing power over its customers.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

Balance Sheet

The board has been able to grow the equity value at a 7.89% CAGR in the last 10 years. Instead, the intangible assets and Goodwill now represent almost 10% of the total assets, against 4% in 2014 which is a very healthy value.

The firm has managed to keep an average of 6% interest rate since 2018. This translates into interest coverage against its EBIT of almost 12 times in 2023. These facts, together with the low 2023 Net Debt / EBIT ratio of 0.417 draw a very robust picture for the group regarding its balance sheet.

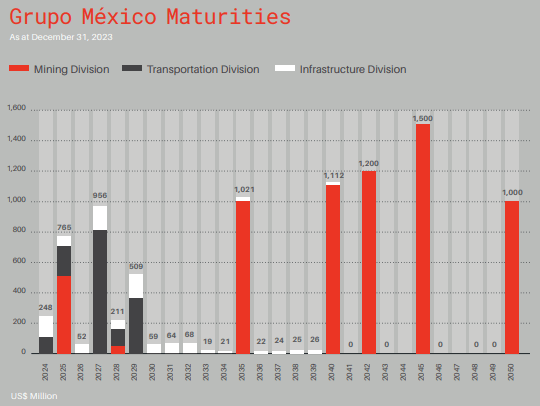

The debt maturities calendar shows a positive view into the future as in the next 10 years, payments are all below 1000 million US dollars and the group managed in the last 5 years to generate an average free cash flow of 3184 million US dollars per year. Therefore, the next debt maturities are well covered by the firm cash flow generation capacity.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

The liquidity ratios also indicate a healthy short-term horizon for the firm, with the Acid Ratio above 4 and the Quick Ratio almost at 5.

Cash Flow Statement

For 2023, the group invested 1910 million US dollars back into its businesses, and for 2024, the firm expects to continue with this level of re-investment with 1970 million US dollars to be deployed into the division’s companies.

Taking a look at the historical records, the firm spent each year in CAPEX and acquisitions 1892 million US dollars on average for the period of the last 10 years. In 2023, this expenditure represented 32.8% of the operating cash flow.

Looking back 10 years, the expenditure cycle of GMEX has been characterized by an explosion in investment in the period between 2006-2012, which matches the copper price rallies that happened during that time. In these 10 years, the CAPEX has decreased at a CAGR of -1.3%. Instead, in 20 years, it has grown at a CAGR of 9.12%

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

GMEX has been rewarding shareholders an average of 5.6% yearly over the last 10 years, although this percentage has been very volatile and subject to the firm results. The dividend has been growing at a CAGR of 11%, and with an average payout ratio of 57% for the same period. The amount of shares in circulation has decreased a 0.43% in 2023 after being flat for the last 10 years.

The operating cash flow has grown at a CAGR rate of 10% for the last 20 years. Instead, the free cash flow has grown at a CAGR of 8.7% for the same period.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

Company’s Key Financial Information

Image created by the author using information from the company´s annual reports (Author’s own Analysis)

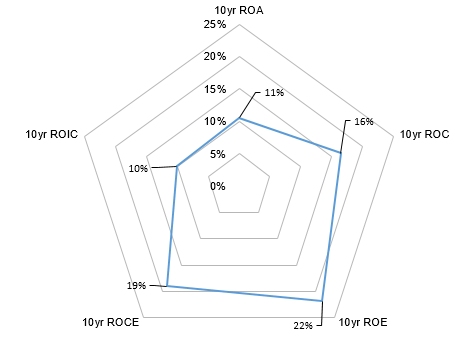

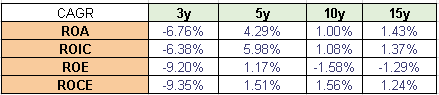

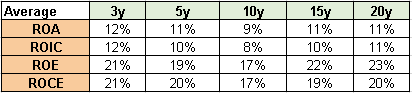

The chart above indicates how, during the last 10 years, the company has delivered an average rate of return over the invested capital of 10% and a return on equity of 22%. This shows how the firm has offered equity holders an excellent return on their investment and also proves how the management has a good track record navigating the cycle with a very decent ROIC for the sector.

Asset Allocation Evaluation

Image created by the author using information from the company´s annual reports (Author’s Own Analysis) Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

It is visible how margins and profitability margins are correlated with the copper price cycle and how they all bottomed in 2015-2016 to recover to their current levels.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis) Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

The tables above show how these profitability ratios have behaved in the past 20 years, which is almost flat. This means that the management has proved to be able to navigate the cycle and provide shareholders with solid and stable returns over a long period.

Growth Metrics

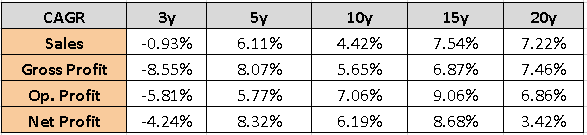

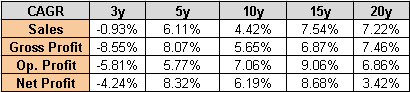

Their revenue, gross, operating, and net profits have grown, as shown in the table below. It is worth mentioning that although sales have tripled in the last 20 years, the group has not been able to capture the full revenue growth and translate it into the bottom line. The table below shows how sales have grown at a CAGR of 7.22%, instead of net income only at 3.42%.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

About growth quality, the company has managed to grow 62% of the time on average in the last 10 years and 60% in the last 20 years showing the cyclical nature of its business operations.

Valuation

Relative Valuation Metrics

Trailing Acomo Multiples

The current price multiple that the market is willing to pay for GMEX is pretty much the same as it was 10 years ago, except for the years when the group’s earnings decreased given the cyclical nature of the commodity prices, where the P/E multiple almost doubled, the firm has traded around 10-13 times for the last 15 years.

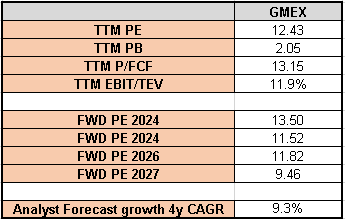

The stock is currently trading at a TTM price-to-earnings P/E of 12.43 and has a dividend yield of 4.68%. The current price-to-book value is 2.05. If we look at the TTM Price to Free Cash Flow P/FCF, it is currently around 13.15.

The 10-year average P/E is 12.37, the dividend yield of 4.42%, the price-to-book value is 1.39 and the P/FCF is 17.3 this means that currently, the stock is trading near its historical valuation.

Forward Multiples:

Currently, analysts forecast an annual growth CAGR rate of around 9.3% until 2027. The expected P/E ratio for the period from 2023 to 2025 is 13.5, 11.52, 11.82, and 9.46 respectively for the current share price. Analysts expect Grupo Mexico to have a strong growth mix, with the usual weaker years linked to the cyclical character of the mining sector.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

Relative Valuation against Industry

Again, GMEX is trading cheaper than its peers in some of the TTM multiples like P/E and EBIT/TEV but more expensive looking at the PB and the P/FCF. On average, I would say that GMEX is currently trading in line with the industry players.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

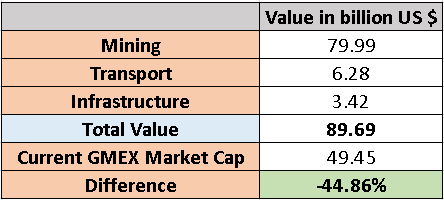

Holding Valuation, Sum of parts

I would like to calculate the value of the holding company by adding the market value of its parts:

-

Mining Division: Grupo Mexico owns 88.9% of Southern Copper Corporation. Today, the market capitalization of this company is 89.99 billion US dollars.

-

Transport Division: Grupo Mexico Transportes is a publicly traded company in the Mexico stock exchange, with a market capitalization is 8.97 billion US dollars. GMEX owns 70.27% of the company.

-

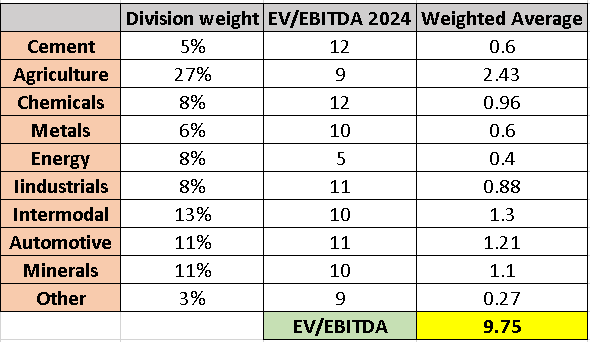

Infrastructure Division: this part of the group is not publicly traded, so I am going to value it with the EV/EBITDA multiple method. I used the EV/EBITDA multiples per industry for emerging markets that NYU’s Aswath Damodaran professor indicates for 2024 on his website.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

In 2023, this division made 350.428 million US dollars, so we can value this segment as 3.416 billion US dollars.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

Let’s now see if this valuation gap matches the historical values:

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

For simplicity, I have not included the infrastructure division, as it has been a relatively small contributor to the group revenue historically. The current undervaluation is slightly higher than the average number of the last 7 years. I do not believe that this gap between the holding market capitalization and the sum of its parts will close in the future. Usually, the holding structure implies a punishment in the valuation of about 25-30% of the sum of the parts. I also assume the market is including a layer of precaution due to FX and country risks.

Discounted Cash Flow Valuation

Calculation assumptions:

-

Revenue growth: as mentioned before, over the last 10 years, GMEX has grown its top line at a CAGR of 4.42%, I believe in the next 10 the group will be able to grow at a higher rate as several tailwinds favor this firm business; therefore, I will apply a growth rate of 6% for the calculation, this value is more in line with the historical 20 years firm’s growth rate.

-

EBIT Margin: as explained before, margins in this company followed the copper price cycle in the last 20 years, and the data indicates that the EBIT margin has oscillated between 30% and 40% depending on the year. I believe that a margin of 35% on average is appropriate.

-

Tax Rate: 30%, is the 2024 Mexican nominal tax rate.

-

Reinvestment Rate: in the last 10 years, the firm has re-invested an average of 1890 million US dollars back into the business with a CAGR of 4%. These values include the big investments or acquisitions that the firm will perform.

-

Investment Rate of Return, IRR: here I do not use the WACC personally, I look for a minimum IRR of at least 15% for the cyclical names, in addition, this higher rate of return reflects the country and operational risks associated with the firm’s business nature.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

Applying the input presented above, the DCF calculation gives a target share price of 74.36 Mexican pesos for investors looking to get a 15% return on their investment.

Sensitivity Analysis

To add an extra layer of precaution, I run a sensitivity analysis to understand the impact of changing the IRR and the rate of growth.

Image created by the author using information from the company´s annual reports (Author’s Own Analysis)

The market is currently pricing a very high growth rate between 9% and 10% or an IRR lower than 13% with lower growth. If investors think that these assumptions are appropriate, the stock would be a buy for them. But, as I will explain in the Risks chapter of this article, I believe that we are heading for the end of this business cycle and commodity prices could suffer a big hit if the global recession fears come true.

Looking Forward

Risks

Operational & Environmental Risks: Mining activities are highly dependent on the right execution and being completely compliant with the environmental policies expressed by the related regulatory entities and local governments. GMEX in 2014, had a spill of copper sulfate into the Sonora River affecting more than 22,000 inhabitants in 8 different Mexican regions. Currently, the Mexican government is running an investigation to assess if this accident was caused by negligence. In that case, the government requested the mining company to complete the remedy plan to combat the environmental damages caused, as the group only paid half of the promised compensation. This past incident is a reminder that even if the company makes all the steps right as until now, there is always the risk of an accident happening in the future.

Regulatory and Political Risks: The mining sector always carries regulatory and political risks that could affect, as shown above, there could be environmental consequences if an accident happens. However, Grupo Mexico is a Mexican company with a long history and expertise, its activities are based mainly in Mexico, where the group has important knowledge of the political and social situation. The company is very aligned and focused on giving back to the Mexican society through its foundation programs that aim to support the local communities, institutions, and environment.

Global Economy Downturn & Commodity Price: As 81% of the group’s net profit in 2023 came from the mining division, and especially from mining copper, GMEX is highly dependent on the global economic activity output to further improve its results. Currently, Asia and especially China is in an internal economic downturn, also fueled by the real-state turmoil, not being able to go back to its historical growth rates after the pandemic. Europe is also on a similar path but caused by the political turmoil and debt levels that the EU countries could face in the following years. On the other hand, the economic exceptionalism of the US could also arrive to an end if the recession fears come true. The price of copper or “doctor” copper, as this commodity price is historically known to be correlated to world economic activity. This cyclical relation could be maximized as the major economies in the world seek to electrify their societies and invest in greener energy production methods. Right now, having cooling global economies can be translated into a lower price of copper as its demand is reduced, and big infrastructure investment plans are delayed into the future.

Future Growth

As mentioned above, what can hurt the copper price now, can help it in the future. The world is determined to electrify their societies. From electric vehicles, and renewal energy, such as solar power and energy storage, to grid modernization and electrification of remote areas. Copper is a key material for upgrading infrastructures, supporting the urbanization of emerging market regions, and being the base for further technological implementation and developments like 5G, the Internet of Things, or artificial intelligence.

All these tailwinds will translate into higher demand for copper even if more supply comes online, as the thirst for this metal will outpace the mining sector’s capacity to bring online additional mines or expansions. As an indication, copper mines take between 12 and 16 years to be online. Also, the amount of regulatory and environmental requirements to be fulfilled by a mining company to bring online a copper mine is very important. This means that big players like GMEX have a moat thanks to its long history, expertise, extensive resources, and reputation in this industry. GMEX is well-placed to capture these tailwinds and translate them into solid future returns for the shareholders.

Conclusion

Grupo Mexico is a very robust player in the mining sector. It also has resilient transportation and infrastructure segments, which will drive future growth to the group thanks to the Nearshoring after the COVID pandemic. This name is poised to benefit from global green policies and the electrification of societies. I believe that the stock trades slightly above fair value, as the heavy reliance on commodity prices for the group’s numbers makes it a cyclical player. The last global economic indicators suggest that the global economy could suffer a cooling in the following months or years; therefore, investors should take a cautious approach towards this sector.

In my opinion, I consider Grupo Mexico as a buy-and-hold name for the long term as the company has very solid and prudent financial management, Tier-1 quality assets, diversified operations in different sectors, promising future growth tailwinds and consistent solid returns to shareholders make it a very compelling candidate.

I recommend readers willing to add this name to their portfolios, first add it to their watchlist. They should await further economic indicators to confirm if a recession or a small bump is in the way and catch the stock with a lower price with enough margin of safety. For investors already in this name, I recommend holding it for the longer term without adding it here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.