{kind=link}

Olemedia

EnerSys Investment thesis

EnerSys (NYSE:ENS), the industrial battery company, showed more revenue shrinkage and earnings growth in its most recent quarterly report.

It is that earnings growth that deserves investor attention, keeping the company in the growth category.

The stock is currently undervalued and I have a one-year price target of $119.24, a 20.97% increase over the closing price on August 28, 2024.

About EnerSys

The company and its predecessors have built industrial batteries for over 125 years. Today, the emphasis is on “stored energy solutions” for industrial applications. Its operations involve four segments, as reported in the 10-K for fiscal 2024 (which ended March 31, 2024):

- Energy Systems: provides uninterruptible power systems for data centers, telecom, switchgear, and electrical controls. These systems are used in industrial facilities, electric utilities, large-scale energy storage, and energy pipelines.

- Motive Power: offers motors for electric industrial forklifts, mining equipment, diesel locomotive starting, and other rail equipment.

- Specialty: this segment builds premium batteries for starting, lighting, and ignition applications for moving vehicles, from large over-the-road trucks to satellites.

- New Ventures: specializes in energy storage and management systems for demand charge reduction, utility back-up power, and dynamic fast charging for electric vehicles.

EnerSys has been an active acquisitor, with 35 acquisitions between 2003 and fiscal 2024. In July 2024, fiscal 2025, it finalized a deal to buy Bren-Tronics for $208 million. In a news release announcing it, Bren-Tronics was described as “a leading manufacturer of highly reliable portable power solutions, including small and large format lithium batteries and charging solutions, for military and defense applications.”

At the end of March, EnerSys had more than 10,000 customers in over 100 countries.

At the close on August 28, shares traded at $98.57 and it had a market cap of $3.98 billion.

Competition and competitive advantages

EnerSys reported in the 10-K that the industrial energy storage market is very competitive. It added that it competes on five factors: reputation, product quality, service reliability, delivery lead time, and price:

- In the Energy Systems segment, the main competitors are East Penn Manufacturing, Exide Technologies, Fiamm, SAFT, and others.

- For Motive Power, the main competitors are East Penn Manufacturing, Exide Technologies, Hoppecke, Eternity, Midac, Sunlight and TAB.

- For Specialty, key competitors include: Clarios, East Penn Manufacturing, Exide Technologies, Fiamm, Banner and Atlas Lithium Corporation (ATLX), Eagle Picher and SAFT.

- New Ventures’ primary competitors are Jule, Tritium DCFC Limited (OTCPK:DCFCQ), and ABB Ltd. (OTCPK:ABBNY).

Through the segments, EnerSys has a long list of competitors, but only a few are publicly traded. This should give it an edge when raising capital.

It also has a competitive advantage through its quality systems, that are based on ISO 9001: 2015. All plants must achieve mandatory certification to that standard, and those that service specific industries such as aerospace and medical devices must attain industry-specific certifications. These quality systems lead to better quality products and lower prices.

EnerSys also holds many patents and patent licenses. However, no individual patent is material to the business, and it depends more on the quality of its products and relationships with customers.

These advantages help it deliver good margins (comparisons with Industrials sector medians):

- Gross margin: 28.30% versus 31.30%.

- EBITDA margin: 14.26% compared to 13.72%.

- Net margin: 7.73% versus 6.16%.

Based on this information, I believe EnerSys has at least a narrow moat.

First quarter, fiscal 2025 results

Delivered on August 7, the EnerSys Q1-2025 earnings report shows it missed revenue estimates by $23.51 million or 6.13%, and beat on Non-GAAP EPS by $0.30. For the quarter that ended June 30, the headline announced its gross margin was 28%, up 160 basis points year over year.

Other data included:

- Net sales: $852.9 million versus $908.6 million.

- Adjusted EBITDA (Non-GAAP): $121.4 million versus $122.2 million.

- Net earnings (GAAP): $70.1 million compared to $66.8 million.

Other results of note:

- Share repurchases: $11.6 million (none in Q1-2024).

- Dividends per share: $0.225 versus $0.175.

- Total capital returned to shareholders: $20.7 million versus $7.1 million.

President and CEO David Shaffer noted, “We delivered EPS as planned by holding price and taking disciplined cost reduction actions while investing in exciting future growth opportunities.”

His remarks about holding prices and disciplined cost reduction are both welcome. Holding prices means the company did not compromise its pricing to generate new business, which keeps margins up. Disciplined cost reductions suggest the company has a plan (no doubt including its quality systems) to lower costs and is sticking to it.

The company summed up its balance sheet and cash flow situation with this slide in the Q1-2025 earnings presentation:

ENS balance sheet and cash information (ENS Q1-2025 investor presentation)

Other notes from the earnings release:

- The gross margin improvement involved increased benefits from the Inflation Reduction Act.

- It closed the acquisition of Bren-Tronics.

- Was in the final testing phase of its first commercially ready Fast Charge & Storage System.

- It continues to move forward on its lithium gigafactory plant and awaits word on the Department of Energy’s funding allocation.

Despite lower revenue, EnerSys grew its basic EPS to $1.74 and its diluted EPS to $1.71; both increased by $0.11 over the same quarter last year. It also repurchased shares, increased the dividend, and continued to develop new opportunities that will lead to more revenue and earnings in the future.

Dividend

As we saw, EnerSys raised its dividend from $0.2250 to $0.2400. Based on the August 28 closing price of $98.57, the current yield is 0.97%.

The payout ratio is a low 10.64% and the annual payout is $0.96, based on the Q1-2025 increase. The Seeking Alpha system gives it an A grade for dividend safety.

Growth prospects

For several consecutive quarters, EnerSys had generated strong revenue growth, but that slowed in the first half of calendar 2024, while EBITDA and net income leveled out:

ENS revenue, EBITDA, net income chart (Seeking Alpha )

As shown on the chart and as we saw above, net income ticked up in the most recent quarter. But is that sustainable growth, and can it continue if revenue keeps heading down?

The company laid out its expected results for fiscal 2025 in the Q1 earnings presentation:

ENS fiscal 2025 guidance (investor presentation)

How do those numbers compare with fiscal 2025 results?

- Revenue for fiscal 2024 was $3.582 billion, so fiscal 2025 revenue of $3.735 would be a contraction of 4.27%. Fiscal 2025 revenue of $3.885 billion would be an increase of 8.46%.

- On the earnings side, adjusted EPS in fiscal 2024 was $8.35. An increase to $8.80 would represent an uptick of 5.39% and an increase to $9.20 would be a 10.18% jump.

For the year as a whole, fiscal 2025 may be a replay of Q1, but on a larger scale. If revenue comes in at the midpoint between the estimates, revenue would grow slightly. For earnings, the midpoint would take growth to the high single digits, which investors would likely find attractive.

The Wall Street analysts see about the same amount of earnings this fiscal year, then serious growth in the following two years:

ENS EPS estimates table (Seeking Alpha )

Intuitively, that makes sense as Bren-Tronics begins making contributions on the top and bottom lines, and its own innovations come online, adding revenue and earnings. Also, we can’t overlook the possibility that EnerSys will make more acquisitions.

Valuation

The following chart shows EnerSys’ price chart over the past decade:

ENS 10-year price chart (Seeking Alpha )

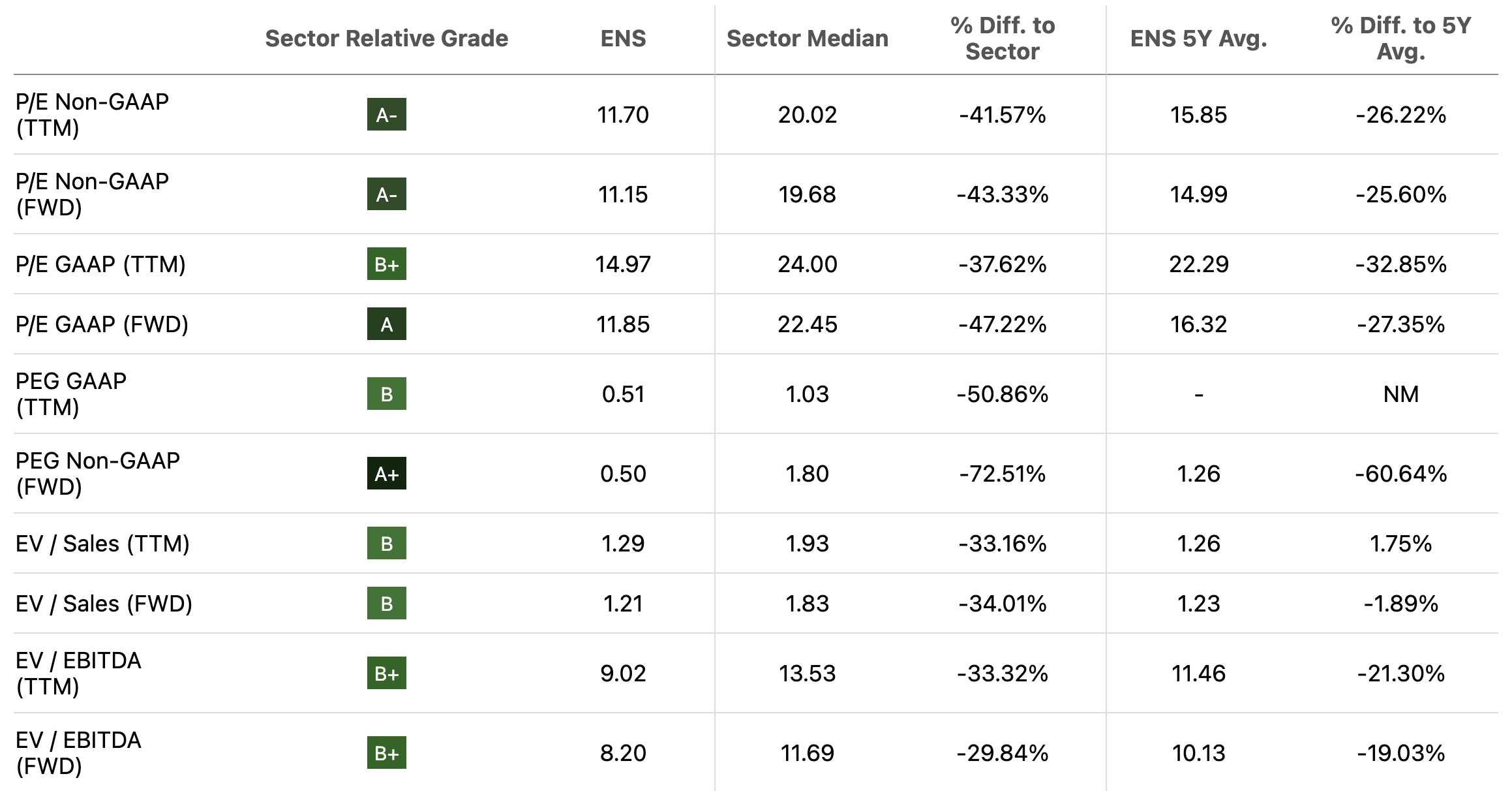

The main metrics for assessing valuation get high grades from the Seeking Alpha system:

ENS valuation ratios (Seeking Alpha )

All ratios here point to undervaluation, and in particular, note that the PEG ratios are well below their Industrials sector medians. Its Price/Sales and Price/Book ratios also fall below their sector medians.

The Wall Street analysts have a one-year target price of $119.24, which would be an increase of 20.97%. That seemed high to me, but I got a different perspective when comparing EPS with the share price on a 10-year chart:

ENS Price & Earnings chart (Seeking Alpha)

Over most of the past decade, the share price has run ahead of earnings, but currently is behind. And not only is the price line below the earnings line, but it appears to be at a low in the sawtooth pattern.

Therefore, I consider EnerSys to be undervalued and a 20.97% target to be reasonable. That’s backed up by five Up revisions and no Down revisions.

It’s also worth noting that 95.45% of common shares are owned by institutions, the so-called “smart money”, although that isn’t always the case. Still, it feels assuring to know that investment professionals are co-owners.

Based on the information above, I too have a one-year price target of $119.24 and rate EnerSys a Buy. The Quant system also gives it one of its relatively rare Buys, while the Wall Street analysts have a collective Hold, based on two Buys and four Holds.

Risk factors

The company has reasonable margins, but it pointed out it operates in a highly competitive industry and is subject to pricing pressures. It added in the 10-K that there is excess capacity in the industry, consolidation among industrial battery buyers, and foreign producers with lower labor costs.

EnerSys operates in a technology-dense environment, and the company has noted, “For certain important and growing markets, including markets served by our Motive Power and Energy Storage business segments, lithium-based battery technologies have a growing market share. Our ability to achieve significant and sustained penetration of key developing markets, including markets served by our Motive Power and Energy Storage business segments, will depend upon our success in developing or acquiring these and other technologies and related raw materials and components, either independently, through joint ventures or through acquisitions.”

Hand-in-hand with new technology is intellectual property, including copyright, trademarks, patents, and trade secrets. A special area of concern is its proprietary knowledge of thin plate pure lead technology, which is not protected by patents.

As an international company, EnerSys has geopolitical and currency risks. That includes the economic circumstances in each of the nations where it operates, trade rules and regulations, global credit markets. Currency risks may help or hinder earnings, but is always an uncertainty.

The company has noted that it processes, stores, and disposes of large amounts of hazardous materials, and especially lead and acid. That exposes it to environmental liabilities, laws and regulations, and the potential for fines, criminal charges, and/or other penalties.

Conclusion

Most often, the EnerSys share price has run ahead of the earnings, but right now it is behind, as well as being cyclically low. That suggests this is a logical entry point for investors looking for an Industrials growth stock.

With new revenue and earnings initiatives ready to kick in, I expect mid-single digit growth in fiscal 2025 and low double-digit growth in fiscal 2026.

I expect the share price to grow almost 21% in the coming year, and rate EnerSys a Buy.