")

{kind=link}

clovercity

If you’re a parent, it’s nearly impossible to not notice the abundance of Crocs shoes whenever you go to the pool, park, or nearly anywhere with children for that matter. This summer, my children have almost exclusively worn Crocs, and I’m sure many other parents can attest to the same.

For this reason, I decided to dig deeper into this company to see if Crocs are more than comfy children’s shoes, I wanted to see if this stock may be worthy of investors’ attention as well.

The Company

Crocs, Inc (NASDAQ:CROX) is a global company that focuses on providing casual lifestyle footwear. The company was founded in 2002 by Scott Seamans, Lyndon Hanson and George Boedecker Jr. The trio had a goal of creating a comfortable, lightweight shoe. The first Croc shoe, called “The Beach” came out in 2002. Although many have dubbed Crocs as ugly shoes, the success of the brand speaks for itself as Crocs soon after became a public company in 2006.

In February 2022, Crocs acquired the HEYDUDE brand. HEYDUDE is a similar footwear brand that is focused on creating causal, comfortable shoes. Their slogan is “Good To Go-To.” HEYDUDE and Crocs are the company’s two current operating segments.

In the last quarter, 35 million pairs of Crocs were sold, in addition to 6 million pairs of HEYDUDE shoes. Crocs certainly has beloved products that consumers enjoy. Let’s next discuss the financial performance of the company and their two brands, Crocs and HEYDUDE.

Financials

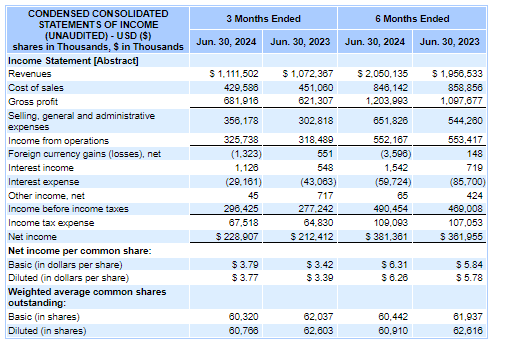

In Q2 2024, Crocs generated revenues of roughly $1,112 million, which is an increase of nearly 5% compared to Q2 2023. For the quarter, the amount of revenue coming from wholesale revenue was slightly higher than direct-to-consumer, 51% to 49%. The direct-to-consumer revenue increased by 10% while wholesale revenue declined by less than 2% compared to the Q2 2023.

For the quarter, adjusted gross margin was 64.1% which is better than 58.1% in Q2 of last year. Operating margin was 29.3% in Q2 2024 which was down slightly, as the operating margin for the prior year second quarter was 30.3%.

These impressive margins led to a higher net income for the quarter and YTD as you can see below:

SEC.gov

I also like that the company has been able to buy back shares, which is helping to grow earnings per share. During the quarter, the company repurchased 1.2 million shares for $175 million. The company has $700 million of share repurchase authorization available.

Turning to their Balance Sheet, Crocs does have enough current assets to cover their current liabilities, which is a positive. However, the company has a significant amount of long-term debt. However, their debt levels have been coming down, as you can see below:

Finchat.io

In the current quarter, the company repaid $200 million of debt, and management has mentioned debt pay down is one of the company’s capital allocation priorities for the current year.

In the current quarter, revenue from Crocs accounted for nearly 80% of the company’s total revenue, while the other 20% came from HEYDUDE. As you can see below, this quarter’s performance is consistent with how both brands have been performing over the last few quarters:

Finchat.io

Let’s next dive into the specifics for each brand.

Crocs

Crocs has certainly been the better performing of the two brands, as this brand generated revenue of $914 million for the quarter, which is an increase of 11% year-over-year. North America revenues increased by roughly 3% and internationally revenues increased by 22% compared to the prior year second quarter. Crocs performed especially well in China, growing over 70% on top of triple digit revenue growth last year.

Management noted having a few successful partnerships this quarter with Pringles as well as Minions, and had success with SpongeBob and Patrick Crocs to celebrate SpongeBob’s 25th anniversary.

The Jibbitz business is doing well for the Crocs brand too as well, as management noted, “The growth of our Jibbitz business during the quarter was led by strong double-digit growth in Asia, which was also our highest penetration by geography. Our Jibbitz consumer continues to be one of our most valuable consumers, and we see them purchasing with higher frequency and average order value.”

Management believes the Crocs brand will grow 3%-5% next quarter and will have growth in the range of 7% to 9% for the full fiscal year.

Next, let’s turn to HEYDUDE, which isn’t performing quite as well.

HEYDUDE

HEYDUDE generated $198 million for the quarter, which is a decrease of over 17% compared to Q2 2023. Management expects HEYDUDE to continue to struggle as they believe revenue will decline 14% to 16% next quarter and believe the brand will be down 8% to 10% for the full 2024 fiscal year.

I think it’s fair to say this brand has under performed since it was acquired in 2022 however as Rees mentioned on the Q2 earnings call, management is still bullish on the long-term prospects of HEYDUDE stating, “…I would say is we are extremely bullish against long-term perspective or projections for HEYDUDE and as bullish as we were when we bought the brand. We, obviously over the last several months it has not performed as we had hoped it would, particularly here in the U.S. marketplace. And I think we’ve talked at some length about some of the things that I think we did wrong associated with that. That does not change our long-term perspective on the brand.”

On the call Rees mentioned the company is focused on engaging the younger female consumer which will hopefully re-energize the brand. I really like the move of signing Sydney Sweeney as the brand’s spokesperson, which will hopefully engage this target audience.

Crocs recently also rehired Terence Riley to help HEYDUDE get back into growth mode. Riley worked at Crocs from 2013 to 2020 and over the past four years worked at Stanley where he turned the drinkware maker into a household name.

Management

Andrew Rees is the current CEO of Crocs. Rees joined Crocs as their President in 2014 and took on the role of CEO in 2017. Rees has more than 25 years of experience in the footwear and retail industry as he previously held various leadership positions at Reebok.

The company’s CFO is Susan Healy who just took over the role in May of this year. Healy has previously held leadership positions at IAA, Inc. as well as Ultra Beauty.

As you can see from these Glassdoor ratings, the company has decent reviews, similar to other retailers such as Foot Locker. Most employees do approve of the job Rees is doing as you can see below:

Glassdoor

Most of my readers will know that I am a big fan of organizations with insider ownership. As stated in the company’s recent proxy filing, Rees does hold 1.64% of the total common stock outstanding, which shows he does have some stake of Crocs.

Risks

In the short term, I think there is some risk of waning consumer demand. In the recent earnings quarter, several retailers including the likes of Etsy (ETSY) and Wayfair (W) noted consumers were tightening their budgets. Nike (NKE) even reported less than stellar results in their prior quarter, although I think their issue is partly due to lack of innovation.

To me, Crocs doesn’t complete with Nike in the same way On (ONON) or Hoka does as Crocs are a cheaper shoe meant for gardening, days at the beach and other causal occasions. For that reason, I don’t think Crocs would be as impacted during times of consumer weakness.

The larger risk to me is that the HEYDUDE acquisition fails, and the company ends up writing off a substantial amount of goodwill, which would significantly impact the company’s income statement. I’m hopeful management can revitalize the HEYDUDE brand but even if they fail to do so, Crocs will survive as 80% of current revenues come from the Crocs brand.

Valuation

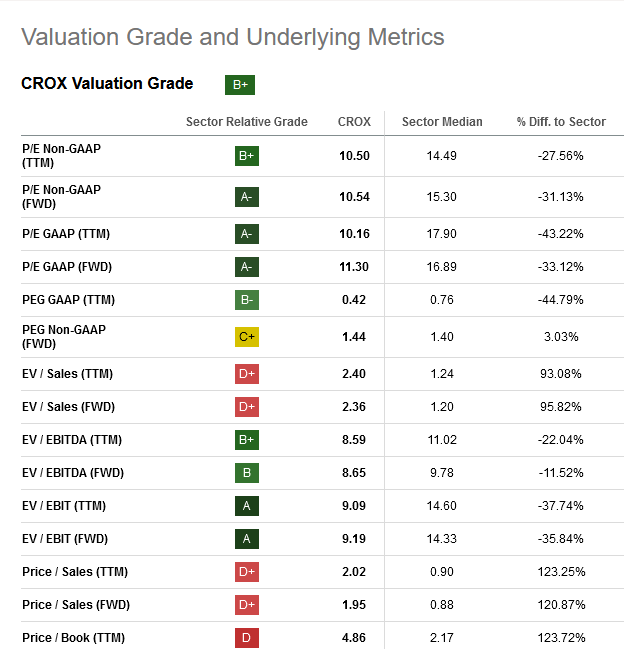

As you can see from the below valuation metrics from Seeking Alpha, the overall value grade for Crocs is a “B+”:

Seeking Alpha

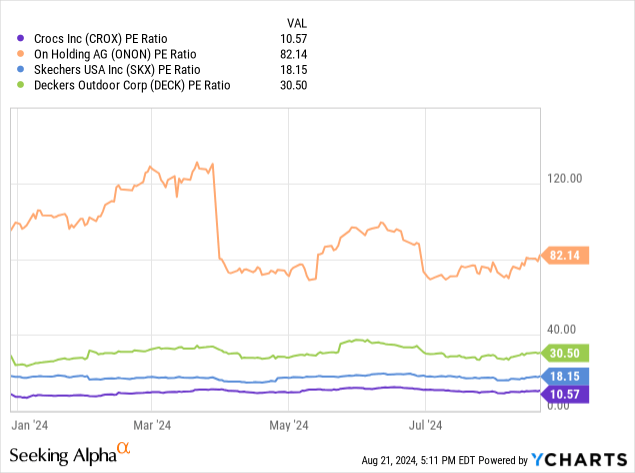

As Crocs is an established, profitable company, I think price to earnings is the best metric to view this organization.

Comparing Crocs to other top footwear stocks with a relatively similar market cap (although DECK has the highest market cap of four), Crocs has a lower P/E ratio than all three competitors despite the continued profits and high margins. This makes me think the stock is undervalued.

Using my reverse discounted cash flow model, I inserted the latest cash flow figures for the company. I used a discounted rate of 10% and a terminal rate of 3%. If you look at analysts’ revenue growth estimates, most are expecting Crocs to have low single digit revenue growth in the years to come:

Seeking alpha

Using a 3% growth rate, which, I believe, is conservative, I come to an estimated intrinsic value of over $217 a share:

Author

Conclusion

I believe Crocs seems undervalued as the market is focusing too much on the under performance of HEYDUDE.

The Crocs brand is performing very well as the brand has been successful with recent partnerships and is growing internationally, especially in China.

I think HEYDUDE can turn things around, and I like the company rehired Riley as he has done an incredible job over at Stanley.

Even though the company has more debt than I would like, management’s decisions to pay down debt and repurchase shares in 2024 is a strategy I think will benefit shareholders.

I feel this not only a beloved shoe for children, but it’s an undervalued gem for investors. Currently, Crocs is a small percentage of my investment portfolio, but I plan to continue to add shares.