{kind=link}

It’s not as big a problem as you might think. The key is to try to mimic the pay-yourself-first approach by setting up an automatic contribution to your registered retirement savings plan (RRSP) to coincide with your payday. A good rule of thumb to strive for is 10% of your gross income. Remember, in most cases the employees blessed with a defined-benefit pension are contributing around the same 10% rate (sometimes more) to their pension plan. You need to match those pensioners stride-for-stride.

How much to save when you’re 40 and have no pension

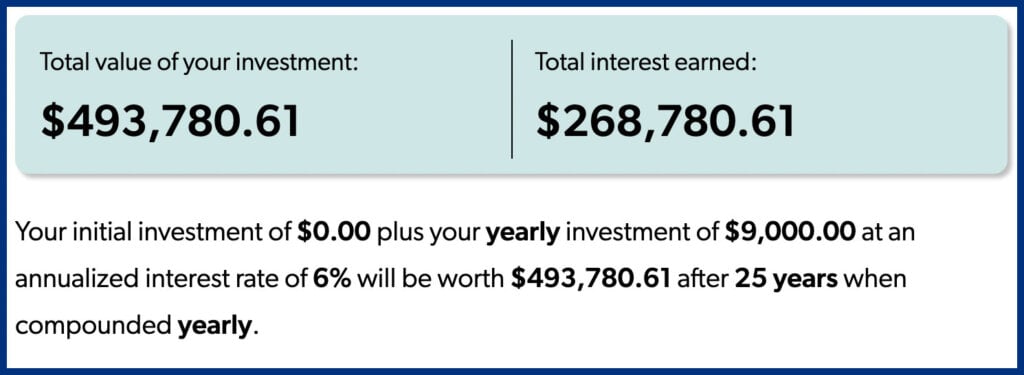

Let’s look at an example of pension-less Johnny, a late starter who prioritized buying a home at age 35 and has not saved a dime for retirement by age 40. Now Johnny is keen to get started and wants to contribute 10% of his $90,000-per-year gross income to invest for retirement.

He does this for 25 years at an annual return of 6% and amasses nearly $500,000 by the time he turns 65.

Keep in mind this doesn’t take any future salary growth into account. For instance, if Johnny’s income increased by 3% annually, and his savings rate continued to be 10% of gross income, the dollar amount of his contributions would climb accordingly each year.

This subtle change boosts Johnny’s RRSP balance to just over $700,000 at age 65.

How government programs can help those without a pension

A $700,000 RRSP—combined with expected benefits from the Canada Pension Plan (CPP) and Old Age Security (OAS)—is enough to maintain the same standard of living in retirement that Johnny enjoyed during his working years.

That’s because when his mortgage is paid off, he’s no longer saving for retirement, and he can expect his tax rate to be much lower in retirement.

CPP and OAS will add nearly $25,000 per year to Johnny’s annual income (in today’s dollars), if he takes his benefits at age 65. Both are guaranteed benefits that are paid for life and indexed to inflation.