: Proceeding From Very Profitable To Embarrassingly Profitable")

{kind=link}

Jeremy Poland

When it comes time for Paramount Resources (OTCPK:PRMRF) (TSX:POU:CA) to rake in the money, this company needs a very big rake. If things keep going the way they are now, the company may need two in the future. This is a company that acquired Apache Canada and has turned those leases into a moneymaker at a level that few companies can compare to. The reason is that this formerly dry gas producer has now focused on rich gas, where the “rich” part is very high-value condensate.

The dividend was raised 20% when the last article came out. However, when condensate is a significant part of the production mix, then the company “has a license to print money” even when natural gas prices decline. This is yet another company that manages to grow production, pay a dividend, and sometimes throw in an extra dividend for good measure. Even doing all that, the bank line remains wide open.

Earnings

While much of the natural gas industry is struggling to get past breakeven, this company had a “relatively” low quarter that many competitors dream of during the boom times.

(Note: Paramount Resources Is A Canadian Company That Reports Using Canadian Dollars Unless Otherwise Stated.)

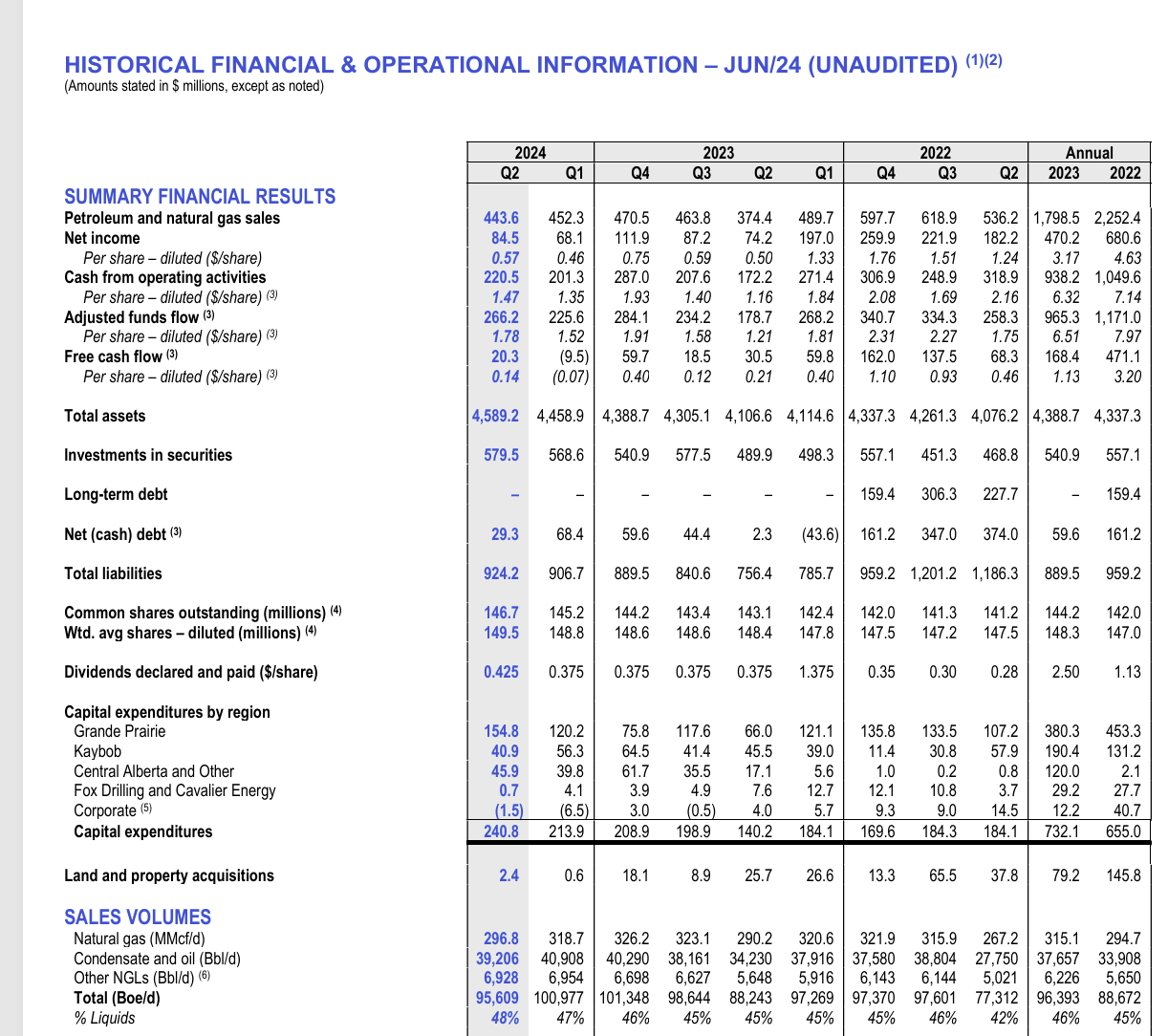

Paramount Resources Summary Of Operations Trend Second Quarter 2024 (Paramount Resources Supplemental Financial Statements Second Quarter 2024)

Note that net income is nearly 19% of revenue. This is happening when much of the industry is waiting for a natural gas pricing recovery. When that happens, that net income percentage will expand as well. Keep in mind that the average corporation reports net income of roughly 5% of sales, and most natural gas companies are struggling to hold the losses down. This company is in a class all its own.

Corresponding to that wide net income percentage is the fact that cash flow is nearly 50% of revenues. By now, it should be dawning on the reader that the wells drilled here are extremely profitable. This is true even when natural gas prices are relatively weak, as they are now.

This is a company that got to a lot of places first before anyone else figured out that the new technology would enable different areas to profitably recover oil and gas. Because it got there first, it has some of the best acreage in North America.

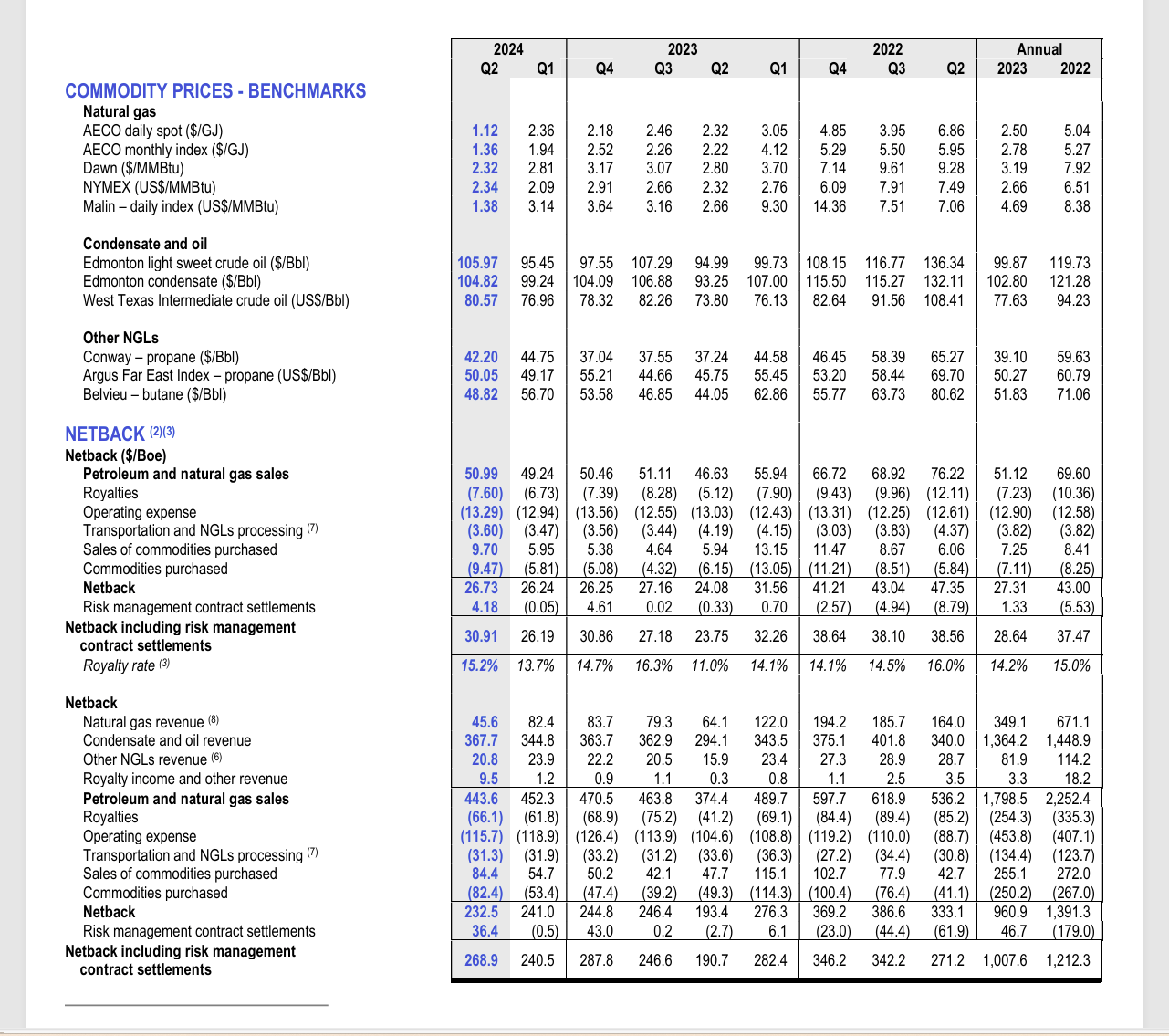

Netback Calculation

The netback remains a huge percentage of revenue because condensate is a premium product in Canada that is worth more than light oil.

Paramount Resources Sales Price Trend And Netback Calculation (Paramount Resources Supplemental Financial Statements Second Quarter 2024)

Even though the condensate is far less than half of the production, it has a clearly outsized effect on the average sales price. Combine that with the per barrel costs that are much closer to a dry gas producer than an oil producer, and the company has a fantastically profitable combination.

While the trend is clearly lower for netback, it is still in a great place compared to many competitors. The cash flood is lower, but it is still a relative cash flood.

Free Cash Flow

Since the company does choose to grow production, that does affect free cash flow. Free cash flow would likely be higher if management elected to just maintain production.

Paramount Resources Free Cash Flow Calculation (Paramount Resources Supplemental Financial Statements Second Quarter 2024)

This is one of the few companies that are financially able to subtract the capital budget from the adjusted funds flow and still has free cash flow even when management decides to spend a lot of money, as they clearly did in the latest quarter.

At the same time, management has noted that they are withholding some dry gas production from the market until natural gas prices recover. That will affect the production reported for the fiscal year. Management has chosen to drill profitable wells while shutting down unprofitable production. If everything that is able to produce is actively produced, then production will grow. Otherwise, the production will come in at the low end of guidance and when natural gas prices recover, there will be an uptick in production.

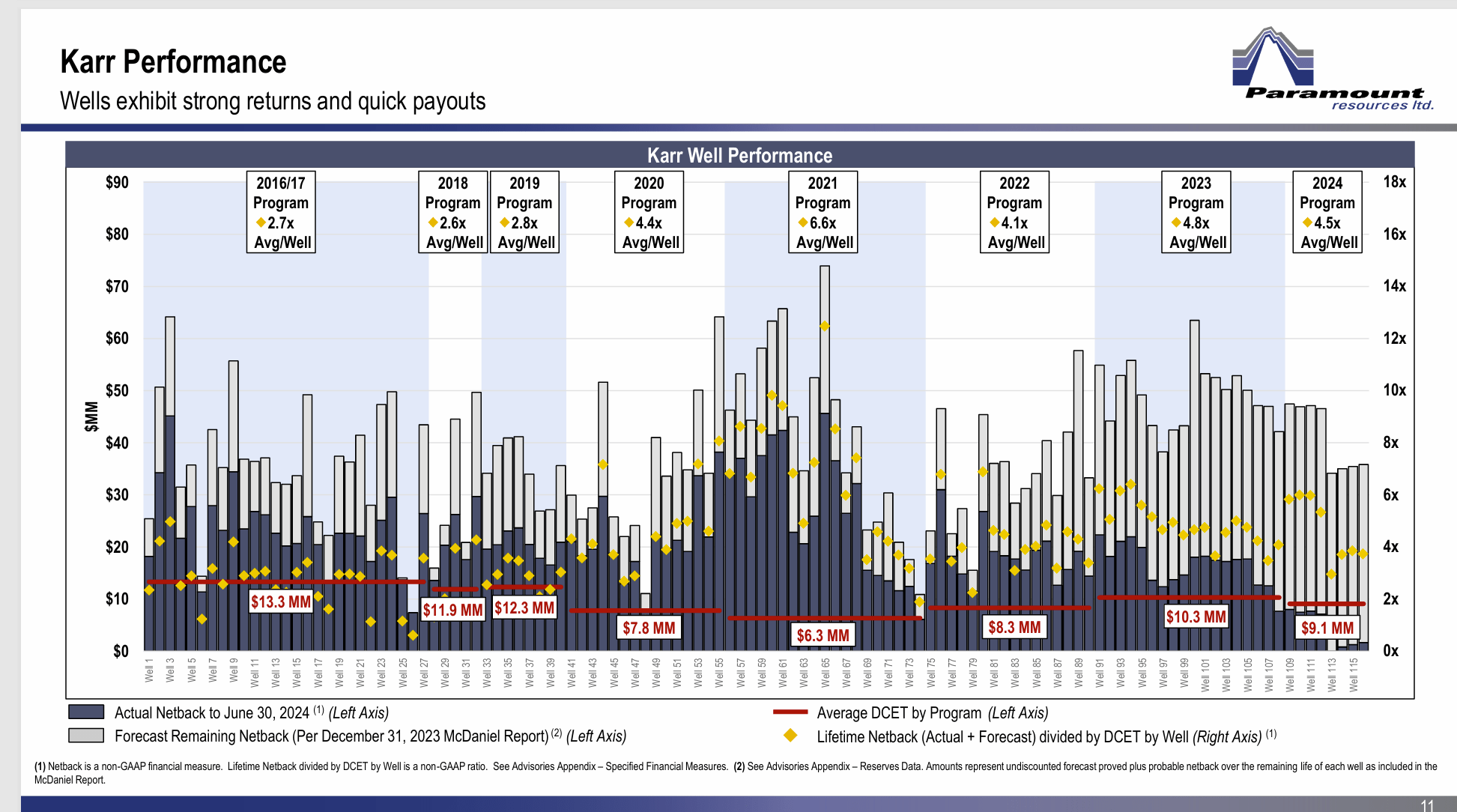

Well Performance

The Karr well performance is shown below. The thing to note is that many of the 2024 wells are already near payback even though this is the second quarter report.

Paramount Resources Karr Well Performance History (Paramount Resources Corporate Presentation August 2024)

Another thing to note is all the paybacks that this company is getting from these wells. In the United States, the most profitable basin is likely the Permian. But the paybacks similar to what is seen here would be a select part of the Permian acreage that a company like Occidental Petroleum (OXY) likely already has under control.

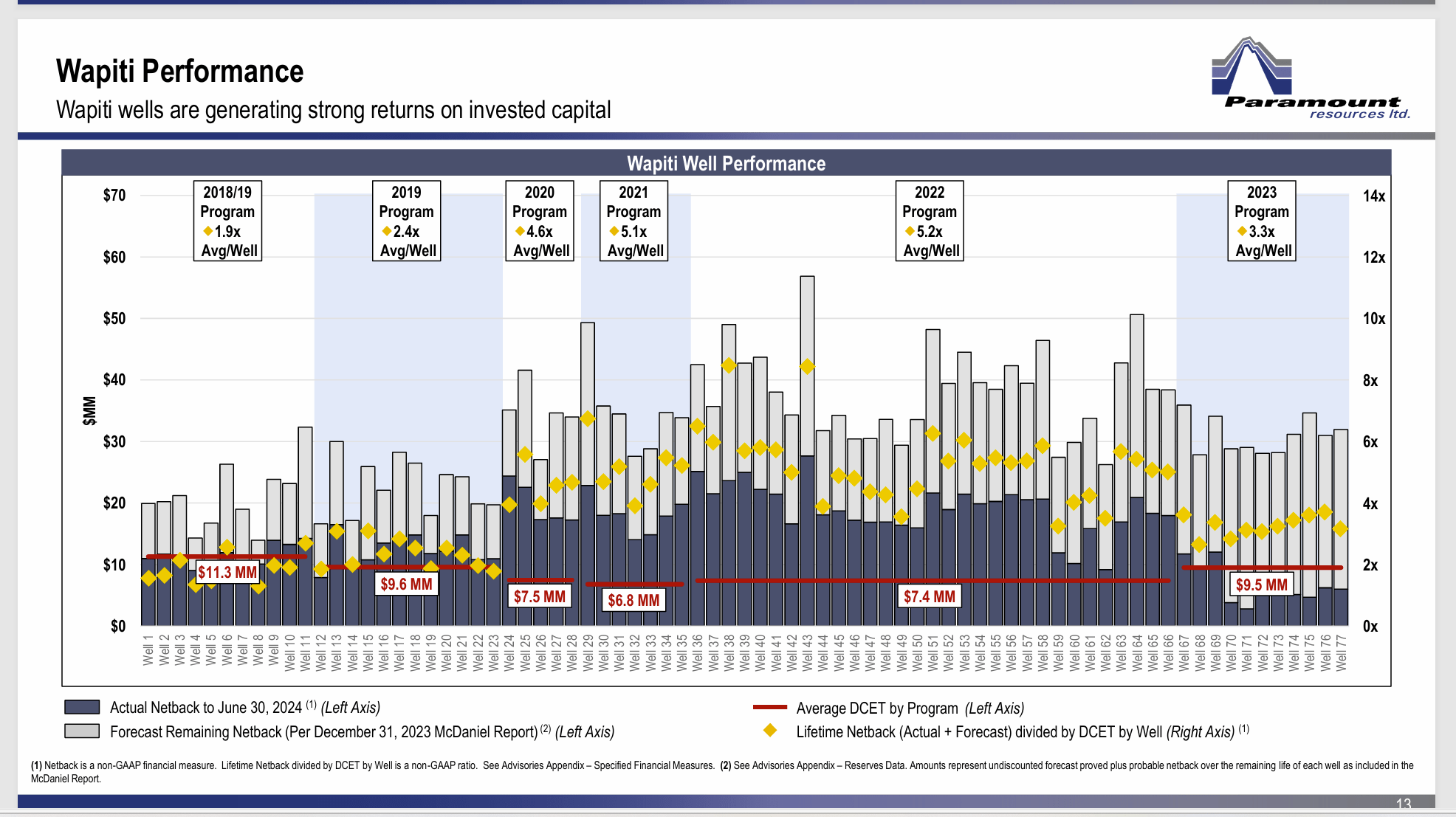

Wapiti

The Wapiti and Karr represent more than half of the company’s production. This gives the investor an idea as to the acreage advantage that this company has over many companies that I follow.

Paramount Resources Wapiti Well Performance History Trend (Paramount Resources Corporate Presentation August 2024)

Clearly this area plus the one before point to some very good well results. This may compare with some of the industry giants in profitability. Very seldom does a company of this size demonstrate wells that are this profitable.

Other Holdings

Besides the obvious operations, this company has holdings in other private and public companies. Sometimes the company will offer to merge with one of these companies. Other times management elects to sell part or all of the holdings. But there is a “sort of” mutual fund operation in addition to the upstream operations.

Summary

By any measure, this company had a great quarter, even if that quarter was lower than some recent earnings reports. Paramount Resources operates at a very different level from most of the upstream companies I follow. It would take quite a downturn for this company to lose money. The rest of the industry would be in far worse shape.

The surprising thing about this is management continues to find new areas that will likely keep the future profitability very high. Paramount Resources continues to be a strong buy. Even if United States investors have to pay the withholding tax (because it is not in a retirement account) this particular company is likely to provide not only good income but also capital gains well into the future.

This is one of very few debt-free companies that I follow that can grow production while paying a dividend. A special dividend and possibly share repurchases may be future considerations. As it is now, the monthly dividend alone is close to yielding what many investors report as a total return.

As a debt-free company, this upstream producer might appeal to conservative investors, despite the volatility of the upstream business in general. Rarely do debt-free companies get into serious trouble. In fact, eventually, this kind of company will normally command a premium to many in the industry as the conservatism becomes known.

The industry is subject to extremely fast-moving and volatile conditions. Therefore, the road ahead could be very bumpy. But the steady growth and the dividend will likely at least double the value of your shares every five years on average.

Oil and gas has been out of favor for some time. That will change down the road. When it does, the price-earnings ratio expansion could offer additional capital appreciation. Typically, companies like this trade for ten to fifteen times earnings in normal (sometimes even boom) times. But the stock is now trading in that range even though earnings are depressed by lower natural gas prices.

With more normal natural gas prices, this is a company that can earn at least C$1 per quarter and up to $1.50 per quarter depending upon the liquids pricing at the same time. The steady production growth will likewise influence that possibility for the better as time advances.

Risks

This is a family-run company that tends to be financially conservative. The founder (who passed away some time ago) was definitely not as conservative. However, should this strategy change, it could change the risk level of the investment.

Any upstream company is subject to the volatility and low visibility of upstream prices. A severe and sustained commodity price decline can change the company’s outlook. The strong finances ensure that this company can shut down unprofitable production while cashing checks for whatever production is sold. Management would then have the option of borrowing to restore production levels should that become necessary.

The family does control enough stock to control the board of directors and the direction of the company. Some public shareholders feel that is a disadvantage. Others like the family control. It is really a personal evaluation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.