")

{kind=link}

tarasov_vl/iStock via Getty Images

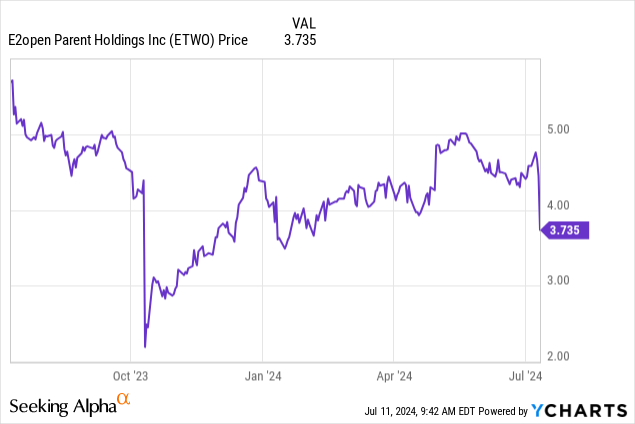

One of the interesting stories we have been following is that of E2open Parent Holdings, Inc. (NYSE:ETWO). As a reminder, this is a stock that we had some nice trading gains in and after locking in gains, we left some profit in the stock as a long-term house position. This is an investing approach that we like because we can capture pieces of all future capital gains, future spinoffs, dividends, etc.

Now, that said, business slowed markedly in 2023 as revenue growth dried up. In our last few pieces discussing performance, it seemed the stock was making a comeback, and new management was orchestrating a turn around. While the stock remains down from its former glory days, the company’s strategic review to improve performance and efficiency is now under the microscope. We further think operations and the depressed price make it a possible takeover target, especially with activists getting involved. However, shares are getting hit today, because in the just-reported earnings, sales expectations are expected to be flat according to the outlook. Sales in Q1 also lagged expectations. We continue to rate the stock a hold here, and will discuss earnings.

E2open Parent Holdings Q1 top-line revenues fall despite turnaround efforts

Unfortunately, despite the work to generate a turnaround and spark business, total revenue is still falling, and revenue was worse than expected. Revenue was $151.2 million, down 5.6% from a year ago, and down about $7 million from the sequential quarter. Subscription revenue was $131.4 million, a decrease of 2.6% from the year-ago fiscal Q1, and represented 86.9% of total revenue. Commenting on the quarter in the press release, CEO Andrew Appel stated:

e2open continued to make progress on our multi-quarter plan to return to strong, sustainable organic growth… we are on track for material improvements in retention metrics through the end of FY25. We are prioritizing and investing in e2open’s most important asset – our client relationships – and in Q1, this enabled us to improve client satisfaction and secure long-term contract extensions to support future growth. We closed important new subscription business in Q1, and although we experienced some temporary deal closure delays, we have already closed a number of those delayed deals in June. We remain confident in our strong market position and are moving forward aggressively with our client-focused growth re-acceleration plan

So some of this commentary explains the revenues miss, that closing on some deals that should have closed in Q1 actually was pushed to Q2. However, the guidance for Q2 with this reality was less than we would have expected, and it comes with earnings pressure, though the company remains adjusted EPS profitable.

E2open Parent Holdings margins, earnings, and cash flow in Q1

Gross profit fell with revenues, falling 8.5% from the year-ago period to $72.7 million, and falling nearly $8 million from the sequential quarter. The gross margin dipped to 48.1% from 49.6% last year. Adjusted gross profit margin was also down from last year. It was 67.8% versus 69.0% a year ago. However, this was a 220 basis point decline from the sequential quarter.

On a GAAP basis, the net loss was $42.8 million, but this is an improvement compared to a loss of $360.9 million last year. Adjusted EBITDA fell to $50.7 million, a decrease of 5.7% from last year, and adjusted EBITDA margin was 33.6%, flat from a year ago. Adjusted EPS was just $0.04. So we do not like all of these declining metrics, but it mostly starts at the top line, except for gross margin percentage. Management needs to get a handle on this through its efficiency efforts. Today, the Street lacks confidence and is selling the stock off.

E2open Parent Holdings fiscal 2025 guidance update

Looking ahead to fiscal 2025, guidance was unchanged despite a weak quarter. As such, subscription revenue is expected to land in the range of $532 million to $542 million. This would be flat growth year-over-year at the mid-point. Total revenue is guided at $630 million to $645 million, and that is 0.5% growth at the midpoint. So this means the sales declines should be stopping. Adjusted margins were guided to be 68%-70%, but we would like to really see these at 70% or above. Adjusted EBITDA for fiscal 2025 is expected to be in the range of $215 million to $225 million, reflecting an implied adjusted EBITDA margin in the range of 34% to 35%. This would be flat from fiscal 2024.

That said, the E2open Parent Holdings, Inc. Q2 guide was a bit anemic. Subscription revenue for Q2 2025 was guided at $129 million to $132 million, reflecting a negative 3.1% decline in the middle of this range. Given deal closures were delayed into Q2 from Q1, we expected this to be higher. The Street likely did, too, and that is why shares are getting hit today.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.