{kind=link}

JamesBrey

Realty Income Corporation (NYSE:O), incorporated in 1969 and headquartered in San Diego, CA, owns and net-leases properties mainly to retailers.

I believe that this REIT is worthy of consideration for both income and value portfolios. Its portfolio diversification level and the nature of the leases can provide stable returns over the long term. But more importantly, the shares appear to be undervalued and now the dividend yield is quite attractive considering the track record and coverage. A shift in market perception driven by lower interest rates could also allow investors to realize unusually high total returns in the near term.

Dividend & Capital Growth

O currently pays a monthly dividend of $0.26 per share, resulting in a forward yield of 5.9%. With a payout ratio of 75.72% based on the last quarterly AFFO annualized and the past payment record, it’s reasonable to assume that the yield is attractive and sustainable.

Seeking Alpha

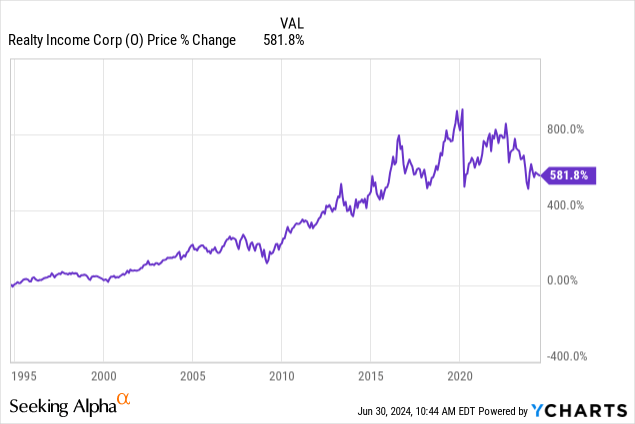

The company also has a long history of delivering value to shareholders through its expansion, as reflected in the long-term growth of its stock price, making it a very good income vehicle:

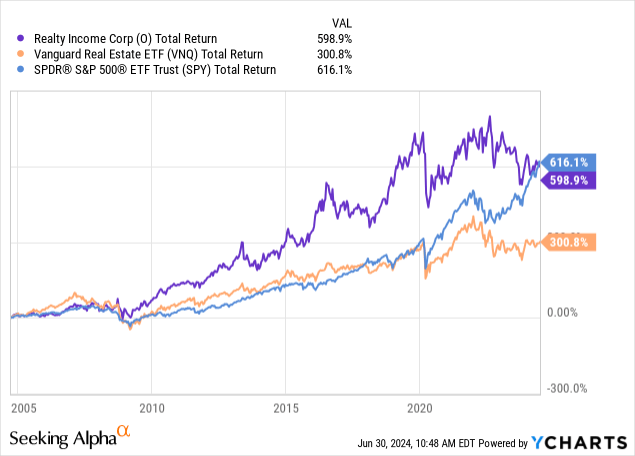

As a result, O has greatly outperformed the real estate market and is only a bit behind the overall equity market as it recently became cheaper and the latter became expensive:

The yield is high enough to make this well-established REIT attractive but, first, let’s take a look at the portfolio.

Portfolio and Leases

The REIT’s portfolio consists of 15,485 properties that aggregate 334,223,900 square feet and are spread all over the U.S., with also exposure to Europe, Alaska, Hawaii, and Puerto Rico. The portfolio is also diversified on a property-type basis. As of the last quarterly report, 79.6% of the portfolio consists of retail properties and 14.7% was industrial, with the rest accommodating gaming, agriculture, office, and country clubs.

I also appreciate that 24.6% of rent comes from grocery stores, convenience stores, and drug stores, which can prove to be resilient revenue sources in adverse periods, providing stability for Realty Income. Additionally, the largest 20 tenants who are responsible for 36.3% of ABR, include large corporations like Dollar General, Walgreens, Dollar Tree, 7-Eleven, and FedEx, with the largest one being Dollar General which accounts for only 3.4% of ABR. The tenant base is clearly as well-diversified as the portfolio. Moreover, at the end of the first quarter, occupancy was very high at 98.6%.

Realty Income net-leases the overwhelming majority of the portfolio, which makes for long-term income generation and low costs; as of the end of the first quarter, the WALT was about 9.8 years and the weighted average rent escalation rate was ~2%. This is the other part of the appeal in O, the first being the attractive dividend frequency and payment record. The reliance on this REIT for monthly income is backed by a timeless need for the services that its tenants provide, as well as lease structures that make for predictability in that income. This reliance is anything but speculative.

Performance & Leverage

Because of the recent merger with Spirit Realty, the YoY rental revenue growth based on the last quarterly results was very high since the addition of Spirit’s revenue to consolidated results during the quarter was responsible for ~55% of the change. Same-property rental revenue increased by 0.76% on a YoY basis which is natural for a net-lease REIT.

| Last Quarter | YoY Change | |

| Total Rental Revenue | $1.2B | 30.57% |

| Same-Store Rental Revenue | $843.4MM | 0.76% |

| AFFO/Share | $1.03 | 5.1% |

AFFO per share increased by 5.1% YoY and this is higher than the management’s currently projected growth rate of 4%, the latter indicating slower growth but nevertheless attractive. This, coupled with the high dividend yield, provides even more proof of the sustainability of the dividend and the prospects for dividend growth.

Now, with credit ratings of A3 and A- by Moody’s and S&P, respectively, the REIT’s cost of debt is very low. That’s not surprising given its low leverage, strong liquidity, and very good interest coverage. The majority of its debt is also unsecured, providing them with great flexibility.

| Unsecured | 99% |

| Fixed-rate | 94% |

| Debt to assets | 37% |

| Debt to EBITDA | 6.11x |

| Interest coverage | 5.2x |

| WAVG Interest Rate | 4.03% |

| Cash and equivalents | $680MM |

| Undrawn Revolver Amount | $3.44B |

| Revoler’s Expansion Feature | $1B |

Also, the maturities are well-scheduled and low amounts are coming due in the next two years:

Investor Presentation

All in all, I think that the long-term outlook is good and the REIT will be able to keep taking advantage of attractive opportunities to expand the business in the short term.

Valuation

Rising interest rates have been hard for REIT stock prices and O is no different; today, the dividend yield of 5.9% represents good value, considering that its 4-year average yield is 4.71% and that the sector median is even lower at 4.32%. Moreover, SPG, KIM, and REG currently offer lower yields and average an FFO multiple of 13x which is higher than Realty Income’s 12.53x:

| Stock | P/FFO |

| O | 12.53 |

| SPG | 11.97 |

| KIM | 12.21 |

| REG | 14.86 |

| Average | 13 |

Considering the growth prospects of the business and dividend, the AFFO yield of 7.8% appears attractive. In fact, in the last earnings call the CEO stated that they expect a ~10% return based on the yield and the AFFO growth. However, if interest rates start decreasing, the short-term returns may be even greater than that as market perception becomes more aligned with Realty Income’s fundamentals.

Risks

Because of the diversification level of this REIT’s business and the good stock price, there are no significant risks for those who are looking for a long-term income vehicle that is going to more than preserve their capital.

However, interest rates may stay high for too long and since there are more undervalued REITs out there that offer higher but sustainable yields, this represents an opportunity risk in the shorter term for those who are looking for more than a sustainable income stream.

And though there is no overreliance on any single tenant here, if something were to adversely affect retailers in general, the additional risk perceived by the market could drive the price lower. Shareholders who intend to buy and hold should monitor the market to better interpret the price changes of O and prevent themselves from making hasty decisions.

Verdict

It’s fairly obvious that the prospects greatly outweigh the risks for Realty Income. As a result of the low valuation, investors could realize double-digit returns based on AFFO expectations, a high yield, and the prospect of lower interest rates. For these reasons, I am rating O stock a buy.

What do you think? Do you own this REIT or intend to? Let me know and I’ll get back to you soon. Also, please leave a comment if you found this post useful; it means a lot! Thank you for reading.