")

{kind=link}

tolgart/E+ via Getty Images

Introduction

A few weeks ago I was analyzing the Invesco S&P MidCap Momentum ETF (XMMO) and saw that its top performer was a company called Vistra (NYSE:VST) of which I knew nothing and discovered that it was an electric power generator investing aggressively into renewables and nuclear power. The electric energy sector is a key theme for me and I have been searching for companies that can benefit from warmer weather, data center demand as well as the transition to EVs. The main drawbacks to a regulated utility are the high capex, long lead times, and regulated returns that can be less than fulfilling. Fortunately, VST seems to be a better fit.

Performance

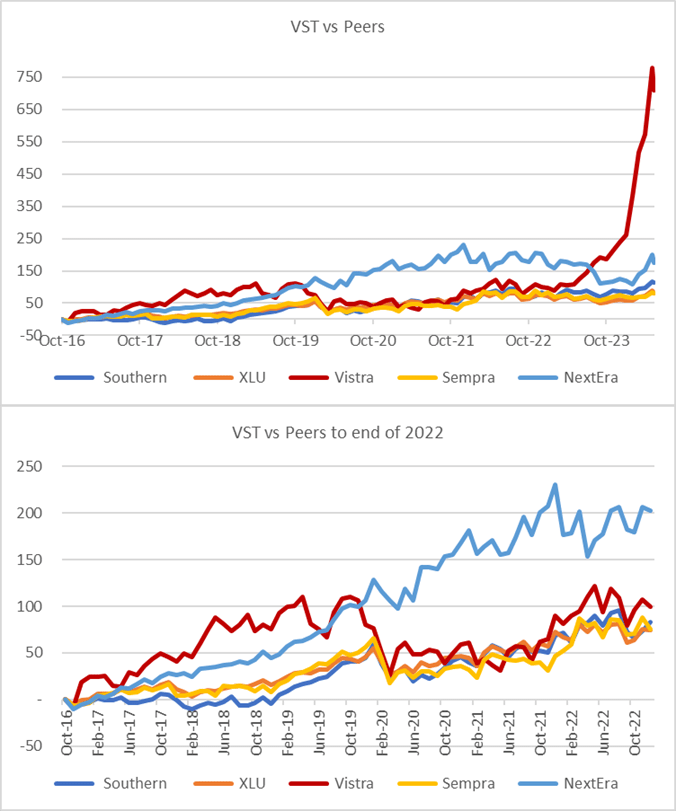

VST has dramatically outperformed (adjusted for dividends) the Utilities Select Sector SPDR Fund ETF (XLU) and selected peers. However, to be fair, this has occurred principally from the start of 2023 to the present. In the next chart, I compared the performance of VST from IPO to the end of 2022 and as can be seen, the stock moved more or less in line with the peer group. The cause of this outperformance, in the last 18 months, is due to the normalization of margins, high share buybacks, and the acquisition of Energy Harbor.

Created by author with data from Capital IQ

What is Vistra

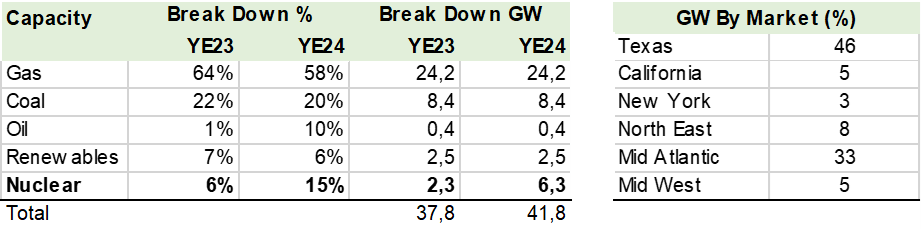

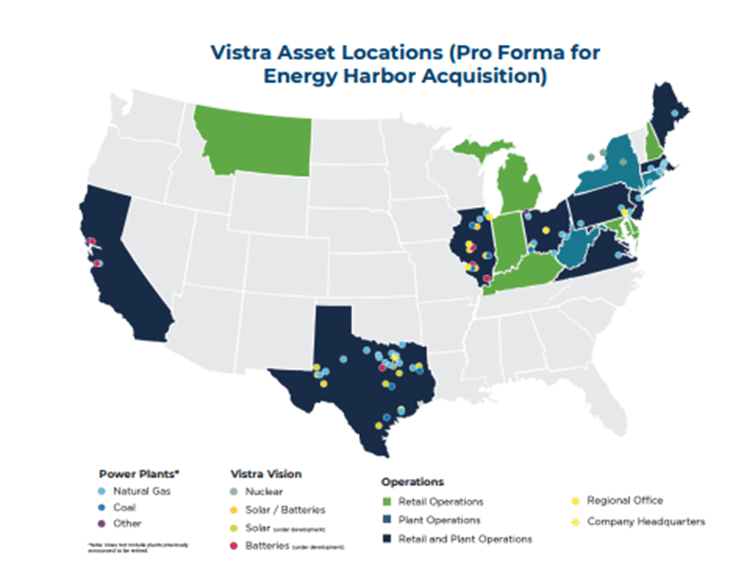

The company traces its origins to the Dallas Electric Lighting Company and over 100 years of M&A, private equity management, and Chapter 11 reorganizations that culminated with the 2016 IPO of Vistra. The company has 41.8GW of capacity spread across seven wholesale markets where it sells electricity to its predominantly business client base. Vistra is an independent power producer (IPP) and not a regulated electric utility. This means that it needs to hedge price and fuel cost or take margin risk.

Created by author with data from Vistra Vistra

Hedging Prices and Fuel Costs

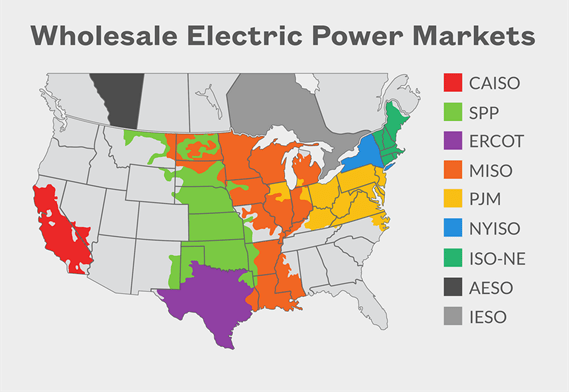

The US has 6 grid systems and 9 wholesale markets that vary in interconnection capacity, resulting in different price systems with demand and input costs creating volatility for the IPPs that sell their energy on a daily price basis. This is why Vistra has hedged (page 19) its sales prices and natural gas inputs through 2026, i.e. locked them in to avoid significant price fluctuations and achieve consistent margins. Thus, cash flow and earnings growth are dependent on demand/volume vs. increased energy price gains despite the general view of higher prices, especially as the US heads into the hot summer climate.

The main risk, as seen in the Texas Uri storm in 2021, is when the company was unable to generate electricity and was forced to buy expensive energy on the spot market. The Texas grid is isolated and difficult to draw energy from other grids, exasperating the price volatility.

EIA

Nuclear Benefits

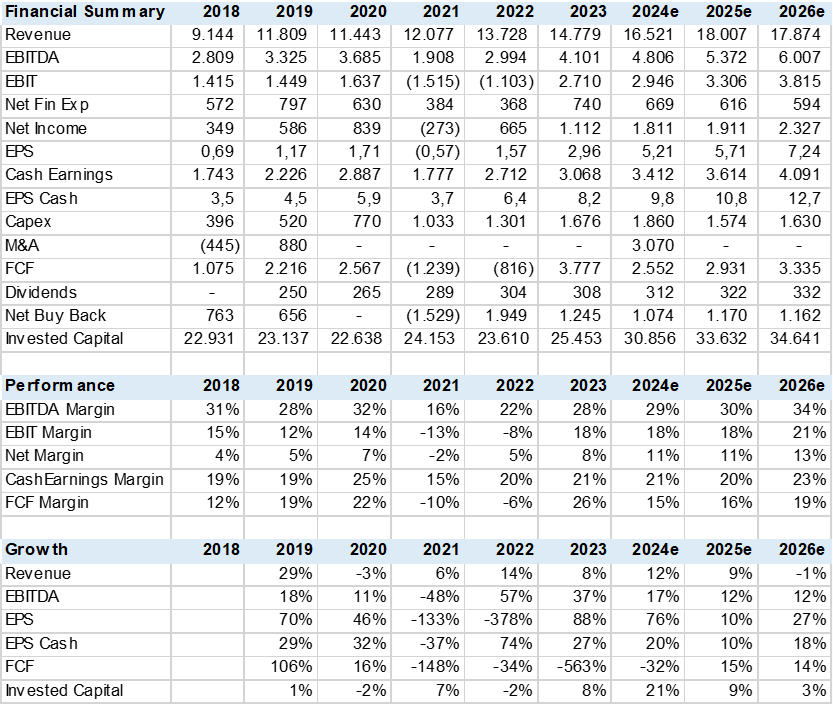

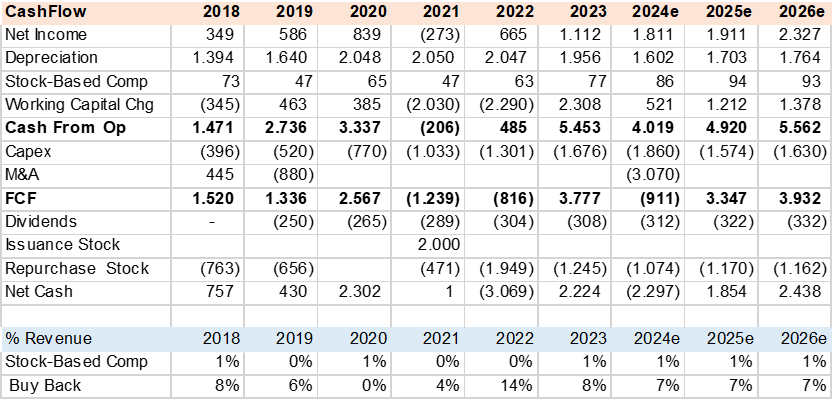

Consensus estimates (10 analysts) incorporate the Energy Harbor acquisition, (consolidated April 2024) which should add US$2bn in revenue and US$575m to EBITDA plus US$125m in synergies in the full year 2025. Post-acquisition the company increases its nuclear capacity by 3x to 15% of the total GWs which should result in higher margins given the lower operating costs of nuclear power plants where fuel is approximately 10% of opex. This nuclear addition may allow the company to close coal/natural gas plants, further improving margins and green footprint.

The consensus forecast indicates EBITDA margin expansion to 34% in 2026 from 28% in 2023, which drives cash earnings growth of over 12%. This in turn provides cashflow to continue US$1.2bn and US$300m in buybacks and dividends equivalent to a 4% yield.

The company paid US$3.5bn (equity plus assumed debt) for Energy Harbor at an estimated 7x EV/EBITDA vs VTS’s 9x today, which, also, creates value. In addition, the company is funding the deal with a debt cost of 7% that may be restructured when/ if rates decline, adding greater investment return.

Consensus Forecast (Created by author with data from Capital IQ) Created by author with data from Capital IQ

Valuation

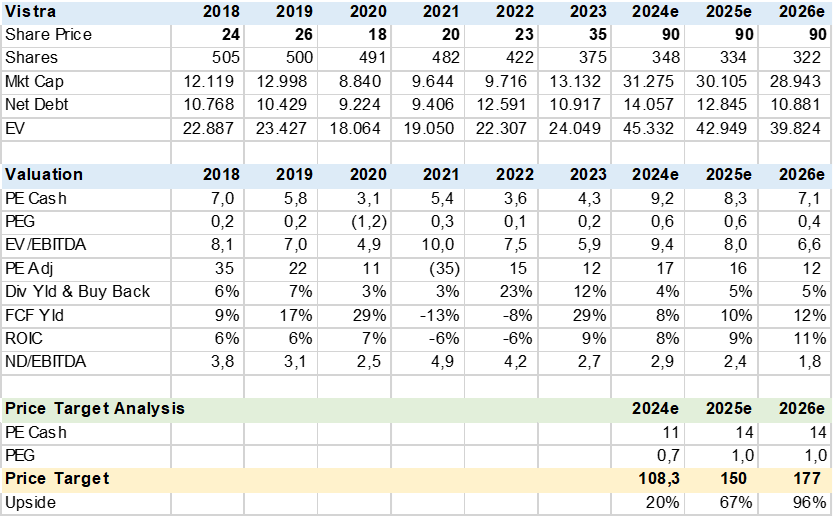

Vistra is inexpensive despite the massive outperformance due to increased estimates driven by the Energy Harbor acquisition as well as growing electricity demand. I prefer to value heavy fixed asset companies on a cash earnings metric. Cash earnings are calculated by adding depreciation to normalized net income, this factors in interest and tax expenses. As can be seen, the stock trades at 9.2x P/Cash earnings per share (CEPS) or at a PEG of 0.6x, which I consider undervalued.

The consensus price target of US$108 backs into a P/CEPS of 11x or 0.7x PEG, which is very reasonable. I believe that Vistra has room for multiple expansions if it can deliver on Energy Harbor synergies and continue to generate positive free cash flow that permits share buybacks and dividends. A 1x PEG on CEPS could drive PE to 14x and a target price of US$150.

Vistra Valuation (Created by author with data from Capital IQ)

Peer Comps

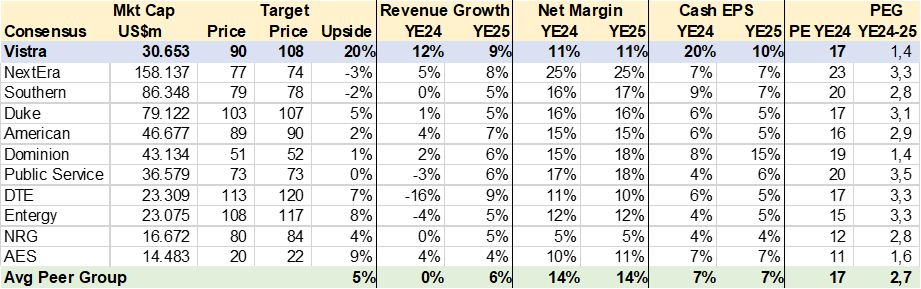

I gathered consensus estimates for 10 peers to better gauge Vistra’s valuation. As with Vistra, I used Cash EPS (net income plus depreciation) as the primary valuation metric. As can be seen in the table below, the stock is cheap relative to growth at 1.4x PEG vs peer average of 2.7x. This is further borne out by the market price target upside potential that is substantially lower than VST.

Created by author with data from Capital IQ

Conclusion

I rate Vistra a BUY. The independent energy company has the right mix of strategy, execution, cash generation, and valuation in a sector that promises to have strong demand in the long term driven by the energy transition to electrification, global warming, and AI data center expansion. It would not be a shock for a larger utility to acquire the company in the future.