{kind=link}

Andrii Yalanskyi/iStock via Getty Images

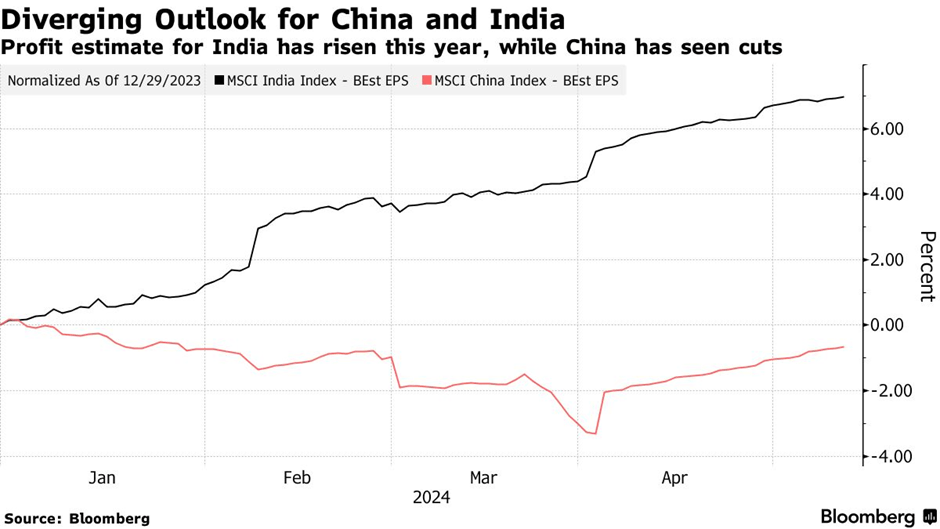

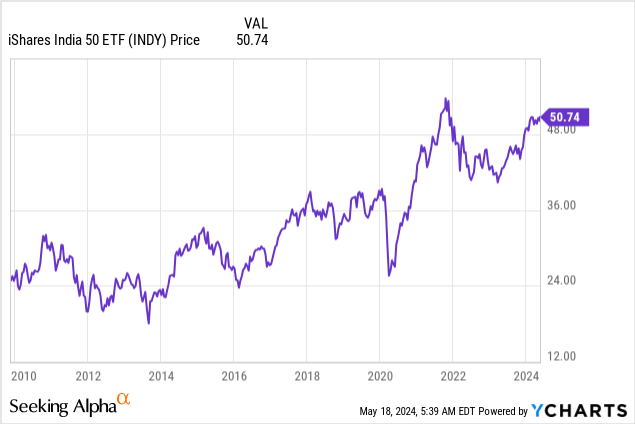

India’s benchmark Nifty 50, which tracks the country’s fifty largest stocks (i.e., the uber caps), has continued its march higher since I last covered its US-listed tracker fund, iShares’ India 50 ETF (NASDAQ:INDY) (see INDY: No Stopping India’s Nifty 50 Stocks Into 2024). Last week saw some jitters creep into the market, however, ahead of election results – despite some very positive macro data (strongly expansionary PMIs, benign inflation prints) and upward earnings revisions at the micro level.

Bloomberg

One potential trigger for the de-rate is news of a lower-than-expected voter turnout this election cycle. Yet, it’s worth noting that polling continues to point in the other direction, with the incumbent government poised to not only return to power but to do so with a much bigger majority than before. So the key question, in my view, isn’t so much whether Prime Minister Modi wins but whether his coalition achieves its 400-seat target. The recent pullback suggests that contrary to what many market watchers expect, a bigger majority for PM Modi isn’t fully priced in; equity upside may therefore still be on the cards post-election.

In any case, the long-term Indian growth story is here to stay. Nifty 50 companies’ through-cycle earnings power remains among the strongest in Asia, along with their underlying return on capital profiles. Backing the earnings runway (currently in the low to mid-teens % through 2024/2025) is an economy that could well outpace its base case >10% nominal GDP growth – if we see the government double down on market-friendly reforms and capex over the next five years. Having lagged the smaller caps through most of last year, an uber cap ‘catch up’ is overdue, and INDY stands out as a key beneficiary.

INDY Overview – Tracking India’s Flagship Stock Index

Among the many Indian large-cap ETFs listed on the market today, the iShares India 50 ETF stands out as being among the few to track India’s flagship Nifty 50 stock index. For context, the Nifty 50 is a market capitalization-weighted collection of India’s fifty largest and most liquid uber-caps.

Fundamentally, though, there isn’t anything particularly special about INDY beyond the index it tracks. Large-cap alternatives like iShares’ MSCI India tracker (INDA) (see INDA: Brace For India’s Post-Election Upside) and Franklin Templeton’s FTSE India ETF (see FLIN: Ride This Ultra Low-Cost ETF Into India’s General Elections), for instance, offer much lower expense ratios.

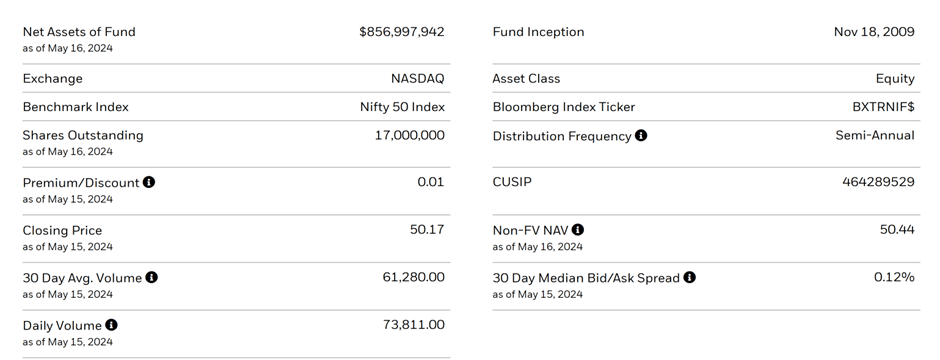

Similarly, its equal-weighted comparable, the First Trust India NIFTY 50 Equal Weight ETF (NFTY) (see NFTY: Equal Weight Is The Best Weight For Indian Stocks), has INDY beat on fees. After factoring in liquidity, on the other hand, INDY, which currently manages a larger $857m and maintains a fairly tight 0.12% bid/ask spread, remains the lowest cost US-listed Nifty 50 tracker.

iShares

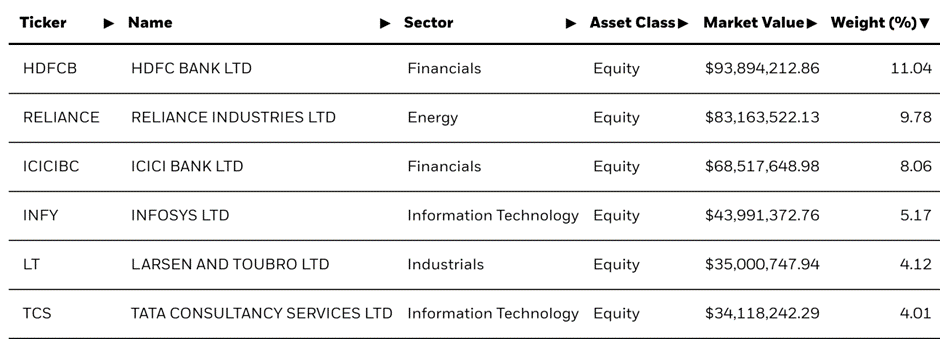

INDY Portfolio – Highly Concentrated on India’s Biggest Franchises

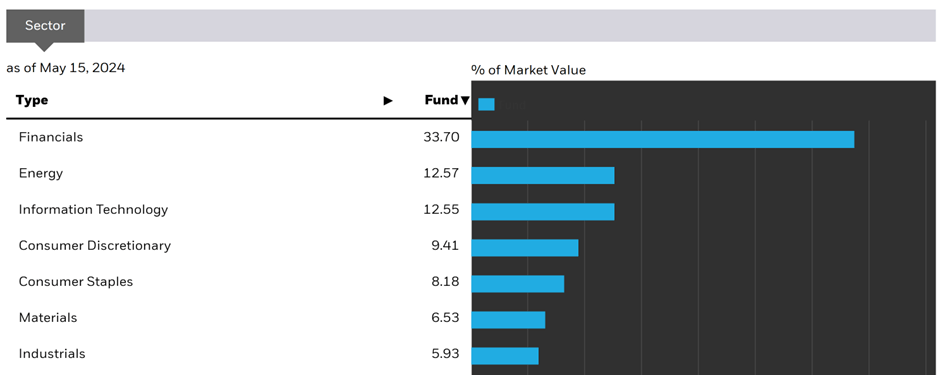

Because it tracks a narrower fifty stock index, INDY is a lot more concentrated at both sector and single-stock levels. Financials remains the leading sector allocation, albeit at a smaller 33.7%, while Energy is now the second largest sector at 12.6%. INDY’s relatively higher exposure to Information Technology has worked against it over the last quarter, and the resulting underperformance has led to a smaller 12.6% allocation for the sector. Elsewhere, Consumer Discretionary (9.4%) and Staples (8.2%) swap places following their Q4 FY24 earnings results. While INDY’s top five sector contribution is slightly down from last quarter at ~76% of the total portfolio, there’s still a lot more concentration here than at comparable large-cap trackers, so investors should be mindful of the risk.

iShares

As for INDY’s single-stock holdings, both leading Indian banks, HDFC Bank (HDB) and ICICI Bank (IBN), top the list, albeit at a reduced 11.0% and 8.1%, respectively. IT services company Infosys (INFY) has similarly lost ground at 5.2%, while the second-largest holding, diversified conglomerate Reliance Industries (RLNIY), is broadly unchanged at 9.8%. On balance, the top five concentration has been reduced by about three percentage points, but remains much higher than other India ETFs. Thus, INDY makes sense for investors looking to double down on India’s largest franchises; those who favor a more balanced approach, on the other hand, will probably find more to like in equal-weighted NFTY or broader Indian portfolios like INDA (136 holdings) and FLIN (229 holdings).

iShares

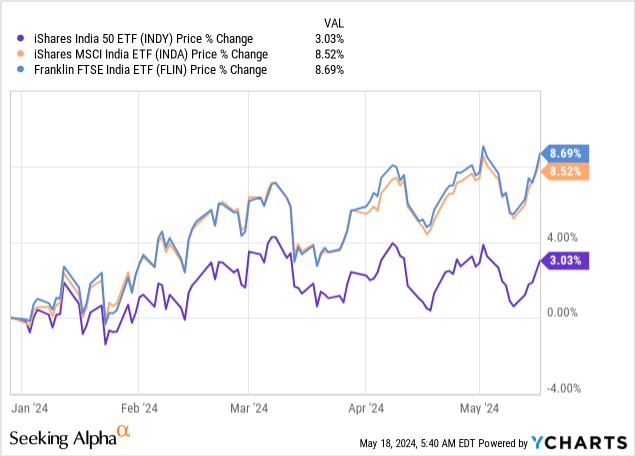

INDY Performance – A Relative Laggard, but There Are Silver Linings

On an absolute basis, INDY has delivered some very strong returns since its 2009 inception (+6.2% annualized). A lot of that return came in the last five to ten years as well, reflecting the extent to which INDY has benefited from the incumbent government’s rule. The issue is that INDY has also lagged the broader Indian ETF space in recent years – compared to INDY’s +18.7%, the equal-weight NFTY delivered +28.5% over the last year, while FLIN and INDA returned +32.5% and +27.4%, respectively. These periods of relative out/underperformance tend to balance out over time, though, as INDY’s superior ten-year track record shows. So, having lost ground in recent years, the more concentrated INDY might be due for a ‘catch up’ soon.

Another positive for INDY is its narrow tracking error (by Indian ETF standards). Yes, the fund gave up over five percentage points of performance vs the Nifty 50 index last year. But large-cap trackers like INDA and FLIN, as well as the other US-listed Nifty 50 tracker, NFTY, gave up even more.

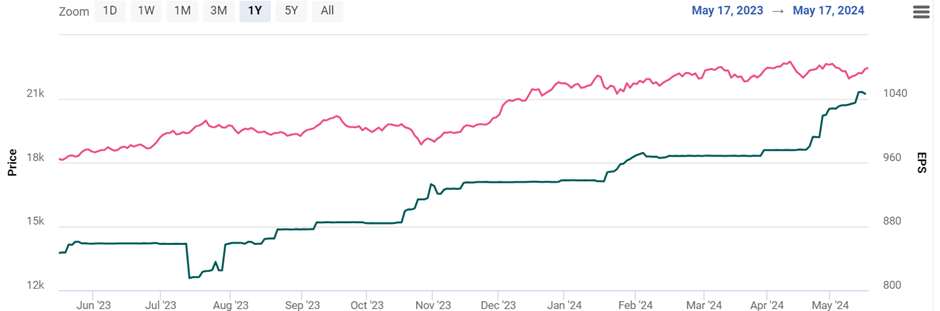

Finally, the INDY portfolio is priced a few turns lower on P/E than other India trackers – despite maintaining a similar low to mid-teens % growth outlook (see converging Nifty price to earnings gap per graphic below). It also offers a very low equity beta (i.e., sensitivity to the broader market) at 0.5 – by virtue of its banking overweight. So for more defensive, value-oriented investors, INDY ranks highly within the India ETF universe.

Trendlyne

India’s Lagging Uber Caps Are Worth A Look

India’s Nifty 50 has seen its year-to-date rally paused somewhat amid earnings season volatility and election jitters as we enter the final stretch. Given polls still point to a market-friendly outcome in the form of a larger majority for the incumbent government, I’m not too worried on this front. Even if we do see a tail risk outcome where the incumbent government falls short, there’s more than enough momentum for nominal GDP and earnings growth to run at well over 10% for the years to come. Relative to the growth potential and capital efficiency of its large-cap holdings, INDY still has ample room to grow into its valuation, in my view. Having lagged behind comparable India trackers recently, the more concentrated INDY presents a compelling ‘catch up’ trade at current levels.