{kind=link}

blackred

I am sure we will have more corrections in 2024, but as far as the April edition is concerned, it appears to be over, with the Fed Chairman sounding dovish in his FOMC press conference last week, and the April jobs report coming in not too hot.

The Treasury market cooperated with the 10-year yield hitting 4.45% on Friday. The week before, we ran all the way up to 4.74%, with corresponding pressure on stocks.

Just as we appeared destined to make a run for 5% on the 10-year Treasury yield, Powell, to his credit, stood in front of the present bond yield spike (note: he failed to do that last fall, when we made it to 5%).

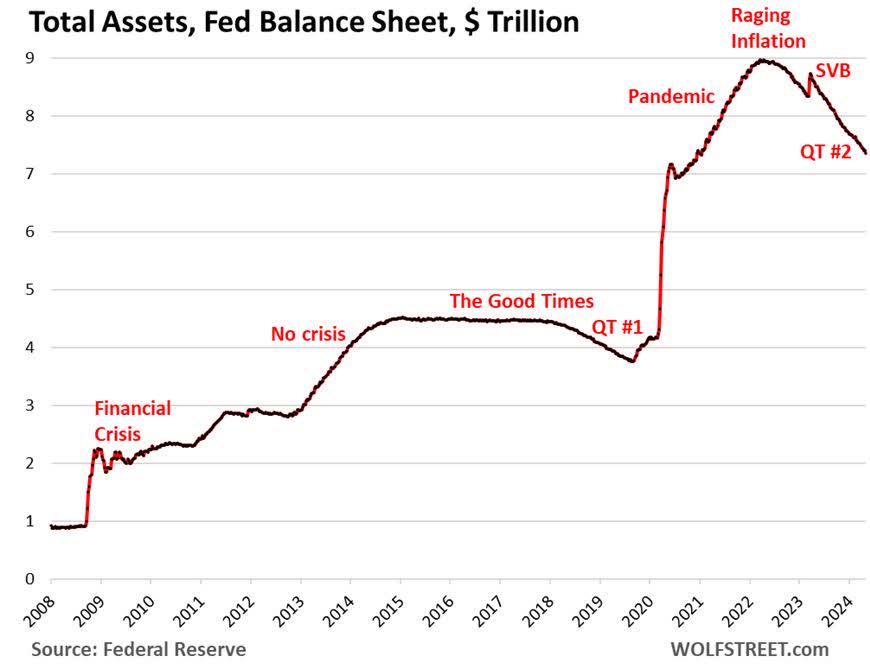

In contrast, the current FOMC statement was crystal clear: “Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage‑backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities.”

So not only is the Treasury runoff rate cut by more than half, but the extra MBS money is also going into Treasuries. Clearly, the Fed is targeting lowering long-term Treasury yields.

Lower rates of quantitative tightening (QT) can be viewed as QE (easing), as it means more electronic dollars in the financial system, which in and of itself has been known to boost both bond and stock prices.

Remember how in 2020 the S&P 500 appreciated 18.4% (with dividends) while the EPS for that index shrank by about the same amount. Typically, shrinking earnings translate to shrinking share prices, but because the Fed was engaging in COVID-era pedal-to-the-metal quantitative easing, which stabilized at $120 billion per month after the initial mammoth surge, the stock market went up as earnings contracted.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

It is widely (but erroneously) accepted that the Fed, acting alone, caused horrific inflation by printing too much money. The Fed did do turbo QE, compared to Ben Bernanke’s tamer version, but inflation came from extreme levels of deficit spending, monetized by the Fed, so the blame must be evenly split with the federal government and Congress.

Basically, Powell did QE for the people, when many were getting paid not to work in a partially-shut-down COVID economy, while Bernanke did QE for the banks, primarily liquefying the financial system. Supply chain bottlenecks added fuel to the inflation fire in Powell’s case.

The inflation we experienced post-COVID is very similar to what happened with the surge in deficit spending for WW2 and the resulting surge in inflation in 1946-1947, when the U.S. economy began to normalize. After it normalized, inflation declined notably, due to saner government spending levels.

So, if Treasuries can stay under 4.50% and we keep getting decent economic data without any dramatic developments on the geopolitical front – which are impossible to predict ahead of time – most likely, equities are headed to new highs.

There is still time for Jerome Powell to get two rate cuts into the system before the election, most likely in the July and August-September periods, which should be cheered by stocks, but he needs the inflation data to cooperate, and that very well may happen given that we are moving away from the bad inflation seasonality in the first quarter when companies tend to raise prices.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Furthermore, when unsure if the stock market is on a firm footing, there is one company’s stock that is leveraged to the well-being of financial markets and the economy, and that is Goldman Sachs (GS). Goldman simply does not do well in a bad stock market, so what is Goldman doing now? All-time high.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Morgan Stanley (MS) is also doing well, but this arch-rival is no longer as leveraged to capital markets because of its huge move towards wealth management, which is a much more stable business, so if one were looking for a leveraged play on capital markets, Goldman’s stock is an indicator, in and of itself.

I think we are headed to new highs for stocks, geopolitics notwithstanding.

Navellier & Associates does not own Morgan Stanley (MS), or Goldman Sachs Group (GS) in managed accounts. Ivan Martchev does not own Morgan Stanley (MS), or Goldman Sachs Group (GS) personally.

All content above represents the opinion of Ivan Martchev of Navellier & Associates, Inc.

Disclaimer: Please click here for important disclosures located in the “About” section of the Navellier & Associates profile that accompany this article.

Disclosure: *Navellier may hold securities in one or more investment strategies offered to its clients.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.