")

{kind=link}

Editor’s note: Seeking Alpha is proud to welcome Eleceed Capital as a new contributing analyst. You can become one too! Share your best investment idea by submitting your article for review to our editors. Get published, earn money, and unlock exclusive SA Premium access. Click here to find out more »

Luis Alvarez/DigitalVision via Getty Images

Summary

I am positive on GitLab Inc. (NASDAQ:GTLB). My summarized thesis is that GTLB’s leading position and strong sales strategy position it well to capture the large and growing addressable market worth over $40 billion. In particular, I believe its land-and-expand strategy has multiple levers of growth that should support very healthy growth rates in the near term.

Company overview

GTLB is an $8.34 billion market cap company that addresses the need for DevOps software solutions. GTLB’s leading DevOps (Developer + Operations) software platform is designed to unify and centrally manage the fragmented and complex process of software development. The GitLab platform is run on a single application with a single codebase, unified data model, and user interface that spans the entire software development lifecycle. Operationally, GTLB reports subscription and license revenue, with subscriptions representing the majority of sales (87% as of FY24).

GTLB

Large addressable market

GTLB

GTLB addresses a very large market that is worth over $40 billion, based on its own internal analysis, and I expect this opportunity to incrementally expand from here as the broader IT spend by businesses is only going to continue growing due to the digitalization trend. Gartner expects worldwide IT spending to grow by ~7% in 2024, for instance. The implication of a growing IT spending budget is that a higher number of software professionals are needed, which drives the demand for GTLB. For reference, over the past few years, the number of software developers has grown by 20%, in line with the digitalization trend.

Strong go-to-market strategy to drive growth

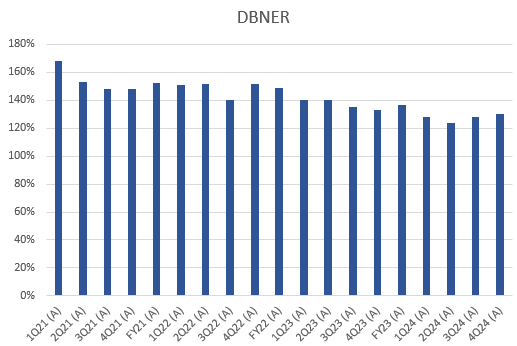

On top of being the leading solution provider, the GTLB land-and-expand go-to-market [GTM] model should drive consistent high growth over the long term. Up until now, most of GTLB’s growth has been driven by customer expansion. The company follows a product-led growth model, first landing smaller customers with its freemium model that includes certain features, and then gradually expanding them to include new users, use-cases, and add-on products. In order to maximize revenue, GTLB is constantly trying to upsell users to more expensive versions of the platform, like the Ultimate Tier, as more features are added. Because of this, a fundamental component of its growth algorithm is linked to these long-term customer expansions, and GTLB has a very strong track record of driving this strategy. This is best demonstrated by the company’s dollar-based net retention rate (DBNRR), which has consistently remained above 20+% over the previous few years (source: GTLB filings, e.g., in the latest 10-K page 7). In order to better explain this metric (as the word “retention” might be misleading), based on the definition of GTLB’s DBNRR, my understanding is a figure above 100% suggests an expansion (same customer cohort spent more with GTLB), and anything below 100% represents a contraction (same customer cohort spent less with GTLB).

The key levers to sustaining this DBNRR (i.e., >100% trend) are mostly going to come from two areas: free-to-paid [FTP] conversion (of existing free users in a paying customer’s organization) and cross/up-sell motion.

We calculate Dollar-Based Net Retention Rate as of a period end by starting with our customers as of the 12 months prior to such period end (“Prior Period ARR”). We then calculate the ARR from these customers as of the current period end (“Current Period ARR”). The calculation of Current Period ARR includes any upsells, price adjustments, user growth within a customer, contraction, and attrition. We then divide the total Current Period ARR by the total Prior Period ARR to arrive at the Dollar-Based Net Retention Rate. GTLB press release

For FTP, GTLB’s offering is geared toward both individual contributors and leaders, with tiers to address each. It targets individuals and small teams with its free offering, which includes all the platform’s base elements. Customers usually choose to upgrade to the paid version when they need to handle a larger team or when the number of users increases. For up-sell, although there is no cap on the number of premium users a customer can have, GitLab can keep upselling customers by encouraging them to upgrade to the Ultimate Tier. That Ultimate Tier’s, GTLB enterprise offering, value proposition to enterprises is huge because it comes with a lot more features and functionalities like increased security, five times the storage capacity, significantly more computing power, and limitless guest users, among many more. In the past, Ultimate cost $100/user/month, which was three times as much as the Premium plan. As of 4Q24, GTLB’s Ultimate tier has transitioned to “enterprise” pricing. For any one customer, all users are priced the same. This effectively “forces” every seat in the company to upgrade to Ultimate-Tier when one of them does (in the past, you could just upgrade two seats, for instance); hence, the pricing step-up is immense. Regarding cross-selling, one lever is to cross-sell adjacent products like Duo Pro for AI and Enterprise Agile Planning for project management, or customers buying more storage and compute power.

Source: Author’s calculation

4Q24 results were solid in my view

In the latest quarter (4Q24), GTLB reported 4Q24 revenue of $163.8 million, higher than the guidance range of $157 million to $158 million and beating the consensus estimate of $157.9 million by 3.7%. Gross profit came in at $150 million, which was also above the $143 million consensus estimate. DBNRR also saw acceleration to 130%, with billings seeing 100 bps of sequential improvement to 33%. In short, I see the results as very encouraging signs that GTLB is still a growing business.

The market did not share my view as the stock plummeted from $75 to the current $52, and I see this as an opportunity. My view is that GTLB continues to execute well against its revenue guidance, and I believe that the share price drop was mainly due to management’s comment that the revenue upside will be more muted going forward. Contrary to how the market perceives this guide, I believe this is a smart guide by management as it is a conservative one that leaves room for upside when the macro environment recovers, which management noted they are already seeing acceleration in the adoption of their platform. This is in line with the DBNRR re-acceleration to 130% from 128% in 3Q24 and the highest number of $100K ARR customer additions in three years.

While the spending environment remains cautious, we believe we are starting to see buying behavior normalize with the accelerated adoption of our DevSecOps platform. 4Q24

Additionally, GTLB is just beginning to tap into the potential of the pricing tier changes that were implemented in January 2021. These changes provide a range of renewal discounts that last for three years. As this new pricing term laps, GTLB will have the opportunity to revisit these contracts and cross-sell or up-sell again, providing another avenue to sustain healthy growth rates.

Valuation

Source: Author’s calculation

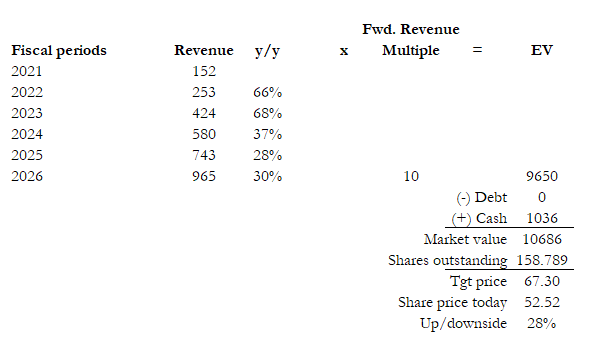

I believe GTLB is worth 28% more than the current share price. My target price is based on FY26’s $965 million revenue and a forward revenue multiple of 10x.

Revenue growth bridge:

I expect GTLB to continue printing healthy growth rates in the future. In FY25, I assumed GTLB to grow at 28%, 200 bps above the midpoint of management FY25 guidance. The logic for this is that management has historically beaten the midpoint of its guide by ~200 bps. This is also in line with my view that the FY25 guide is conservative as it assumes growth deceleration despite the possibility of macro recovery. In FY26, growth should accelerate back to 30% as the economy recovers to a more normalized environment where businesses start to reinvest more in IT spending.

Valuation justification:

Over the past year, GTLB has traded within the range of 8 to 14x forward revenue, with an average of ~10x. I think the stock should trade around 10x vs. the recent 14x because of the evidently lower growth rates (1H24 was growing at 37+%, which is much higher than my FY25/26 estimates).

Investment Risk

Depending on how fast the AI market develops, GTLB might face increasing competition if AI technology is able to revolutionize the way the DevOps department functions. A significant reduction in the need for coding is a very attractive value proposition that businesses will seek to achieve, as it reduces the need to hire strong software developers and subscribe to relevant solutions (like GTLB).

Conclusion

My positive view of GTLB is because of its strong position in the large and growing DevOps market. This leading position combined with its effective land-and-expand sales strategy that leverages a freemium model and tier upgrades, positions it for sustained top-line growth. Recent results and management guidance indicate continued execution and potential upside. Valued at 10x forward revenue, I see a 28% upside to the stock.